Last week, Armstrong Flooring (AFI) reported third quarter results. For background information on the company, refer to my earlier post: https://stockspinoffinvesting.com/armstrong-flooring-stock-spinoff-with-138-upside/

My original investment case for AFI in a nutshell is as follows. AFI sells flooring material which is benefiting from a strong US housing market. While the flooring market has rebounded, it remains 30% below prior peak levels. On the margin front, AFI has much room for improvement. AFI was spun out with EBITDA margins of ~6.0% but management is excellent and has a plan to get margins back to the ~10% range. At the time of the spinoff, the stock traded at an EV/EBITDA multiple of 7.0x while peers traded at ~11.0x. Assuming revenue grows 5% in each of the next three years, EBITDA margins expand to 10% and AFI’s valuation expands to 9.0x EBITDA, the stock will trade for ~$37 (it trades at $18.50 now). Additionally, the flooring market is consolidating. Mohawk Industries, the market leader, has spent $3.5bn on acquisitions and has historically acquired smaller competitors at an EV/Revenue multiple of 1.7x to 2.6x. AFI currently trades at 0.5x.

There were some positives and negatives in the quarter. First the positives….

Margin Expansion

In the quarter, EBITDA grew 25% to $30.4mm, driven by margin expansion. In total, EBITDA margin increased 220bps to 9.7% in the third quarter. This is ahead of expectations and a definite positive.

AFI cited increased productivity and lower input costs as the key drivers of the margin expansion.

Through the first nine months of the year, EBITDA is up 27%. EBITDA margin has expanded 150bps to 7.6%, despite only 2% top line growth. Clearly AFI is making great progress on the margin front. Management’s goal is to get to 10% over the next three to five years. AFI started at 6% margins and is already at 7.6%. Almost halfway to their goal 6 months after the spinoff.

Now the bad news….

Sales Growth

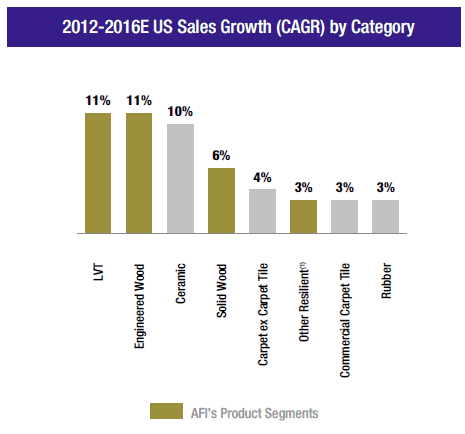

Management’s guidance is for 5% to 6% growth over the medium term (three to five years). According to management, the market grows at 3% and AFI wants to grow ahead of the market through strategic initiatives like focusing on luxury vinyl tile and engineered wood which are growing a lot faster than the market. See chart below:

Source: AFI Investor Relations Website

At the time of the spinoff, management issued 2016 sales guidance for +1% to 6% growth. Revenue grew 10% in the first quarter. In the second quarter, sales declined by 0.4% and management narrowed sales guidance for 2016 to “+2% to +4%”. In the third quarter, AFI saw a sales decrease of 2.0% and decreased sales guidance to “flat to +1%” for the year. Through the first nine months of the year, revenue has grown 2%.

What is causing the pressure on the top line? Management noted competitive pricing pressures and softer end markets. Additionally, AFI saw a drawdown from two retailers. Excluding the drawdowns from the retailers, wood and engineered wood both saw low single digit growth.

Where do we go from here?

It seems to me, the investment thesis is still on track. While revenue growth guidance for the year is now “flat to +1%” it’s still a modest improvement from the last two years. Specifically, sales decreased 3% in 2014 and decreased 1% in 2015. As such, it seems like the turnaround is on track and hopefully revenue growth can continue to accelerate in 2017.

Further, AFI’s margin expansion is very impressive and the midpoint of EBITDA guidance for 2016 has actually improved from $72.5mm to $75.5mm (+4%).

From a macro perspective, the housing market continues to be very strong. On Friday, the Commerce Department announced housing starts increased 26% to 1.323mm in October. Even with the strong growth, housing starts remain below the long term average of 1.442mm, implying a lot more room to run in housing. See my prior AFI post for additional data/graphs on the housing market.

At the beginning of this post, I outlined my original investment thesis which included four years of +5% revenue growth. Given that revenue is on track for 0.5% growth this year (midpoint of guidance), it seems unreasonable to assume 5% growth going forward. Excluding inventory destocking, revenue would have grown ~2% this year. As such, let’s assume revenue increases 2% per year for the next three years (below mgmt’s mid-term goal of 5% to 6%). I will continue to assume AFI can increase its EBITDA margin to 10% over this period, as the company seems to be ahead of plan. These assumptions result in 2019 EBITDA of $129mm. Applying a 9.0x multiple results in an enterprise value of $1.158bn. Backing out net debt and pension obligations results in an expected market cap of $1.104bn and a share price of ~$33. I also assume shares outstanding are 20% higher driven by stock option dilution.

So still good upside, but not quite as compelling at this point.

Currently AFI trades at 7.7x 2016 EBITDA and 0.5x 2016 Revenue, a significant discount to peers which trade at 10.3x and 1.7x, respectively.

If you would like to receive the updated valuation sheet to view AFI’s competitors and their current valuations, click the button below, enter your email address, and we will send it to you instantly.

Leave A Comment