For background on the Nuvectra investment, please refer to my original investment case here:

https://stockspinoffinvesting.com/micrcap-stock-spinoff-trading-below-book-value/

Additionally, there is a very good Value Investor Club write up here:

https://www.valueinvestorsclub.com/idea/NUVECTRA_CORP/138336#description

Short Background

Nuvectra is a neuromodulation platform that was spun out of Greatbatch earlier this year. Nuvectra currently has a market cap of ~$60mm and net cash on the balance sheet of $65mm.

The investment thesis is:

- Management is excellent and has experience in the growing neuromodulation market.

- Nuvectra has an approved product that is growing rapidly and taking share.

- If you believe that Nuvectra’s products will continue to grow and that the stock will ultimately get valued in-line with med tech peers, the stock will be worth multiples of its current share price.

They key takeaway from the Q3 2016 report, is the investment case is on track. The two factors that are most important to me are 1) Algovita sales and 2) sales rep hiring.

Algovita

Algovita is approved for the $1.6bn spinal cord stimulation (SCS) market for chronic pain. It is also expected to be approved for the $500mm sacral nerve stimulation (SCS) market for bladder and bowel control.

What exactly is the Algovita Spinal Cord Stimulation System?

It is an implantable device which delivers steady pulses of energy to certain nerves in and around the spinal cord in order to dull or mask severe pain.

Here’s the Mayo Clinic’s definition for Spinal Cord Stimulation:

“A small wire carries the current from a pulse generator to the nerve fibers of the spinal cord. When turned on, the stimulation feels like a mild tingling in the area where pain is felt. Your pain is reduced because the electrical current interrupts the pain signal from reaching your brain.”

Here’s a great video (~3 minutes) that explains how spinal cord stimulation works to relieve pain:

https://treatingpain.com/treatment/spinal-cord-stimulation

The spinal cord stimulation indication for chronic pain is currently a $1.6bn market. The market is currently made up of four major players: Boston Scientific, St. Jude Medical, Medtronic, and Nevro (newer player).

The neuromodulation platform that was developed at Greatbatch and is now Nuvectra was developed by the technology innovation group within Greatbatch after carefully working with patients and physicians to understand key areas of need. This group has been working since 2009 to develop a differentiated product. The product is finally ready and FDA approved.

What is the sales potential for Algovita?

The spinal cord stimulation market is $1.6bn in size and is growing at 6% per year.

The market is on track to grow to $2bn by 2020. If Algovita can achieve 5% market share, it will ultimately generate ~$100mm of revenue. This seems reasonable if not conservative.

Now back to Algovita quarterly sales.

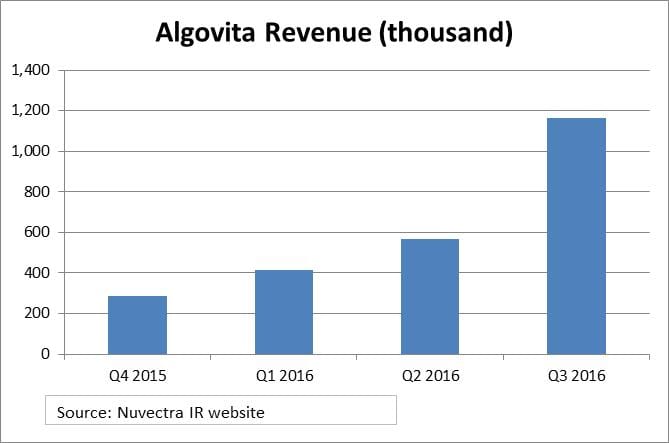

In Q3 2016, Algovita sales increased 105% quarter-over-quarter to $1.165mm, suggesting that the launch is progressing well. Below I’ve displayed the last four quarters of Algovita revenue:

While the absolute dollars are still relatively small, the launch does appear to be on track.

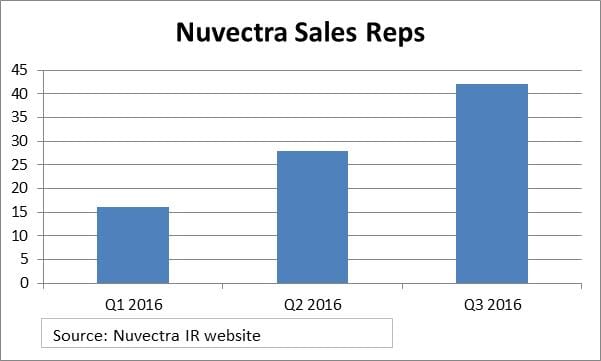

The leading indicator for Algovita sales is the hiring of sales reps. Importantly, NVTR is on track with its hiring plan.

As of November 9, 2016, Nuvectra has hired and trained 42 sales reps. Its goal for the year is 50 sales reps.

See chart below for sales force ramp:

Why is the sales force ramp important?

Nuvectra’s plan is to hire 50 reps by the end of 2016, 100 reps by the end of 2017 and 225 by the end of 2018. Nuvectra believes that each sales rep can ultimately generate $1mm to $1.5mm in annual sales. That productivity implies $225mm to $320mm in sales once its sales force is fully ramped up. If NVTR is able to achieve these targets it will be a great outcome. For reference, consider Nevro, a fast growing neuromodulation peer of NVTR’s. Analysts expect it to generate revenue of $225mm and $320mm in 2016, and 2017, respectively. The company has a market cap of $2.5bn. NVTR’s current market cap is $60mm. Now I’m not saying the NVTR is the next Nevro, but there would be a lot of upside if NVTR continues to progress with its launch. More on this in my valuation section below.

The sales force ramp is also important because sales reps are smart and know the industry a lot better than I do. They would not join a company if they did not believe they could sell the product. During a recent conference, the CEO of Nuvectra described why a sales rep would switch to Nuvectra from another neuromodulation company. The example he gave? Perhaps, that rep’s territory is getting smaller and smaller because his company has hired many sales reps. For that sales rep, it could be a great opportunity to make a lot of money by selling a new product into established relationships that he/she has developed.

Negatives in the Quarter

Were there any negatives in the quarter? Unfortunately, yes, there were.

First, management announced that there was a product recall for one of Nuvectra’s leads. A lead is a wire that connects the device to the patient’s nerve to deliver the shock. I’m still looking into this and will follow up with IR. On the conference call, management noted that this issue was a result of a third party manufacturing issue and has not impacted the roll out of Algovita. They noted that there have been no adverse events. I will report more as I learn more.

The second negative was something I discovered in the 10-Q. In discussing Algovita sales, management wrote: “Additionally, we have expanded our sales management team in an effort to mitigate the challenges we continue to experience in gaining approvals from hospital and ambulatory surgery center purchasing departments.” This wasn’t written in the Q2 10Q and may imply that gaining approval from hospitals and ambulatory center purchasing departments is a little harder than anticipated. However, management didn’t mention anything about the approval process being harder than originally anticipated on the conference call. I will continue to monitor this, but I’m not overly alarmed at this point seeing as the sales ramp continues to progress well.

Valuation

What is Nuvectra worth? I don’t know, but I continue to believe it is probably worth a lot more than its current share price.

I think EV / Sales is the best metric for Nuvectra as it is a rapidly growing med tech company and there is a good set of peer companies.

First, my 2018 revenue estimate. I assume Algovita can generate $50mm in sales in 2018 (ultimately, I believe sales Algovita sales can be much higher than $50mm, but it will take additional years). $50mm in 2018 sales corresponds to 2.5% market share and I believe is reasonable given the sales force ramp.

I estimate $20mm of Virtis (formerly known as Pelvistim) revenue. Please refer to my original write up for the background on Virtis ( I referred to it as Pelvistim as it hadn’t been officially named), but it is a product that is geared towards the sacral nerve stimulation market for bladder and bowel control. The sacral nerve stimulation indication represents a $500mm market that is growing at 10% annually. Nuvectra expects to submit this product for approval by year end.

Finally, I expect Nuvectra’s NeuroNexus unit to generate $5mm in sales. NeuroNexus is on track to generate ~$5mm this year in sales, and I don’t anticipate much growth. This segment is a small portion of Nuvectra that complements its neurostimulation platform.

This all adds up to $75mm of sales in 2018. I believe an appropriate EV / Sales multiple is 3.0x which yields an expected enterprise value of $222mm. Add $20mm of net cash (down from current net cash of $65mm) yields an expected market cap of $242mm. I assume that shares outstanding increase by about 15% to ~11.8mm shares. Dividing the market cap by expected shares outstanding results in a share price of ~$21.

Who knows what the most appropriate multiple is for Nuvectra. Maybe the right EV / Sales multiple is 2.0x. In that case, the stock is worth ~$14. The point is that NVTR is worth significantly more than its current price, assuming the launch goes well and the market rewards the stock with a reasonable peer group multiple.

Click on the link below for additional NVTR valuation analysis:

Click Here for NVTR Valuation Analysis

Judging by Algovita sales to date and the sales force ramp, it appears the stock is on track.

One additional point on Nuvectra from a valuation perspective. The stock currently had a negative enterprise value because the net cash on its balance sheet is greater than its market cap. I recently stumbled upon an analysis of negative enterprise stocks:

The author analyzed 26,569 opportunities to invest in negative enterprise value stocks. He found that those stocks went on to generate an average return of 50.4% over the next twelve months (excluding trading costs, taxes, etc).

The author then published a follow up article titled: Trials and Tribulations of Negative Enterprise Stocks. In the article, he wrote: “The point is that each negative EV stock has something very wrong with it. Most are downright frightening once you start digging into them. This is why they available for sale for less than the cash on their balance sheets. However, despite the fear they inspire, and perhaps because of it, we know that – as a group and over time – they tend to generate highly attractive returns.”

I ran a screen on ycharts.com for medical devices companies with a negative enterprise value. There were only three: NVTR, BIAD, and NSPR. NSPR is $4.4mm market cap company who’s revenue has declined from $6mm in 2011 to $2.3mm in 2015. BIAD is a $1mm market cap company that has no revenue. NSPR and BIAD seem “downright frightening” to borrow the phrase used by the author to describe the typical negative enterprise value stock. What is striking to me, however, is that NVTR is a negative enterprise value stock, but it is not “downright frightening.” It is actually quite compelling. Nuvectra has a deeply experienced team, a newly launched product that is growing 105% quarter-over-quarter, and a new device in the pipeline which will be launched in 2017.

Want to receive our weekly free newsletter that delivers our latest spinoff recommendations and proprietary valuations? Sign up at the link below:

Great write up, many thanks for sharing and shedding light on such a compelling strategy. I’m going to try and value the company myself but was wondering if you have an email address where I can send you that valuation

Do you see any value in their NOL carry forwards? They are valuing them at nearly nothing on the balance sheet as they don’t see them being realised.

I dont know when they expire (they can usually be carried forward for 20 years right?). But there was a note in the recent 10Q that said they were going to continue discounting them like this until they achieve significant profitability. Does this seem extremely conservative, and if so why would they do this?

I noticed that they have to achieve a trailing 6 month revenue of 13.5m in order to access their ‘term loan B’ . Also their agreements with Greatbatch look quite complex but there seems to be some restrictions on them selling large amounts of equity or ceasing operations etc . Are you concerned about their access to liquidity if they don’t hit the revenue target?

I think your observation on NVTR’s

Sorry-having some difficulty getting “approvals” is right on. My understanding is products like these can get tied up for a year in beurocratic red tape, and having people dedicated to this can help significantly. For this reason I am assuming VERY low salesforce productivity for 6-9 months for 2016 and 2017. Management has discouraged people from looking at their salesforce ramp to NVRO for exactly this reason, that is they (NVRO) had a significant number of “feet in the street” before there were ANY units sold (this makes perfect sense) I have a couple of questions/concerns; 1-when will Virtus be submitted for FDA approval?

2-did they hit the “50” rep number at year end 2016? (The presentation on the website says 44 “reps” 1/03/2016 but i think its a typo. 3-there is some (i believe it is post-approval “clinical data due in late February. I am wondering what to look for and any thoughts on this data release.

FWIW, my fieldwork has yielded impressive reports from both docs. and patients and, if the hit 100 reps yay year end 2017, I think they can “crush” your 50m estimate for Algovita. Thanks