Baxter Renal Spinoff Notes

March 19, 2024 Update

Christopher Seto Spectral Medical Inc. – CEO & Director

Scott, so first of all, what I would say is, we’re very pleased with actually the spin-off of Vantive from Baxter and our partnership will be transferred to the Vantive business unit or a company upon completion of their spinoff. It’s still a part of a large entity. So it’s one that generates approximately USD 5 billion in sales annually. While legacy Baxter has been, I’d say, great to deal with and has been a very good partner. Spectral was somewhat of a smaller fish in a big pond. And sometimes, it felt like there were a lot of other projects and interest that we were competing with for Baxter resources. With Vantive and since they’ve announced the Vantive spin-off, we feel that Spectral has been positioned as a key strategic priority. We’ve seen this in Baxter’s investor presentations where both EA and PMX are key featured product launches for Vantive.

Also, when you look at the portfolio of products within Vantive, PMX definitely has significantly higher growth potential and significantly enhanced gross margins relative to their other products. And that’s the nature of our PMX product. It’s unique. It’s not a commodity. There’s no alternatives. And if we get this right, PMX will be the standard of care for ESS and the US ICU population. And I think these are the characteristics that really excite Vantive and ultimately drive the enthusiasm and support that we have witnessed to date. So overall, we feel we’re very important in — well — we feel we were very important in the legacy Baxter world. Our association with Vantive feels like that importance is certainly amplified, if you will.

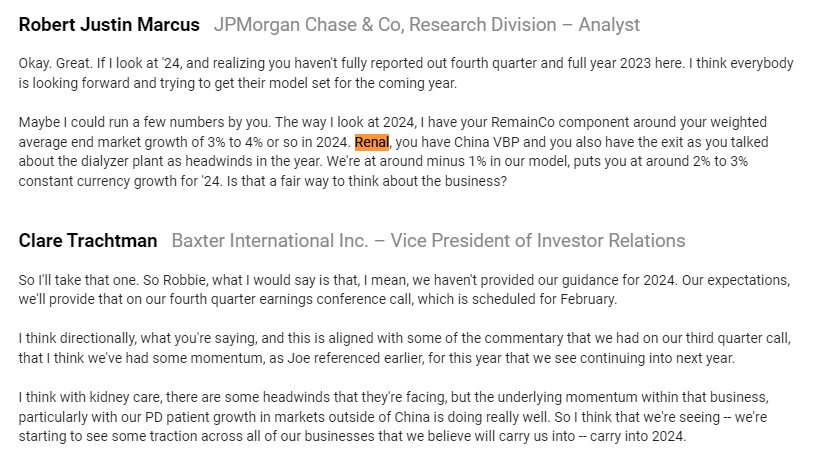

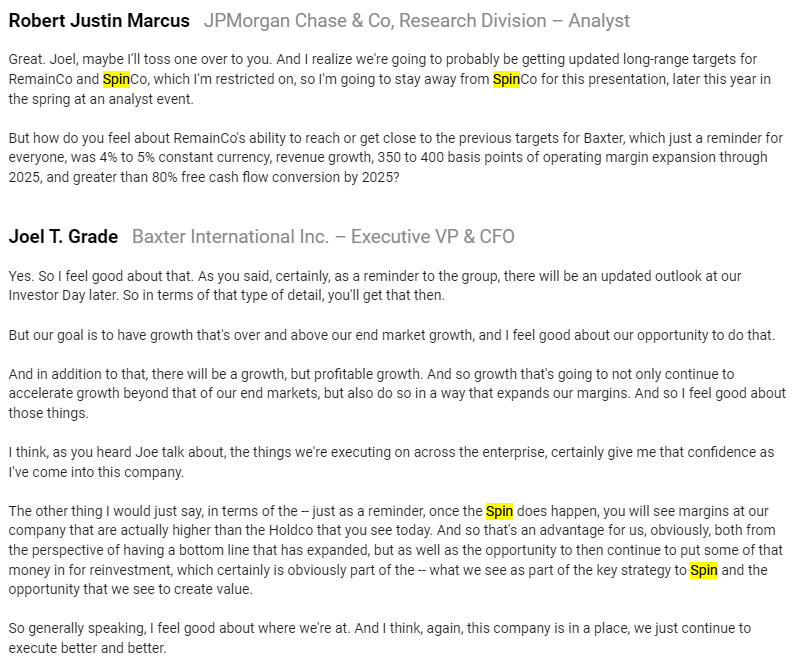

January 18, 2024 Update

This commentary is from the JPMorgan healthcare conference in January 2023:

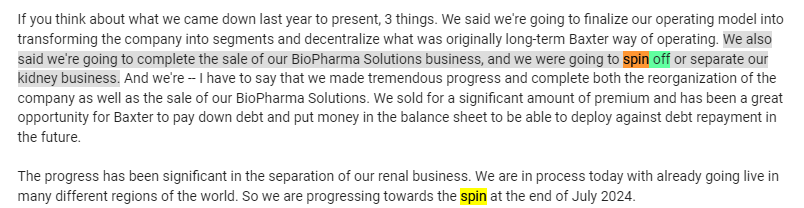

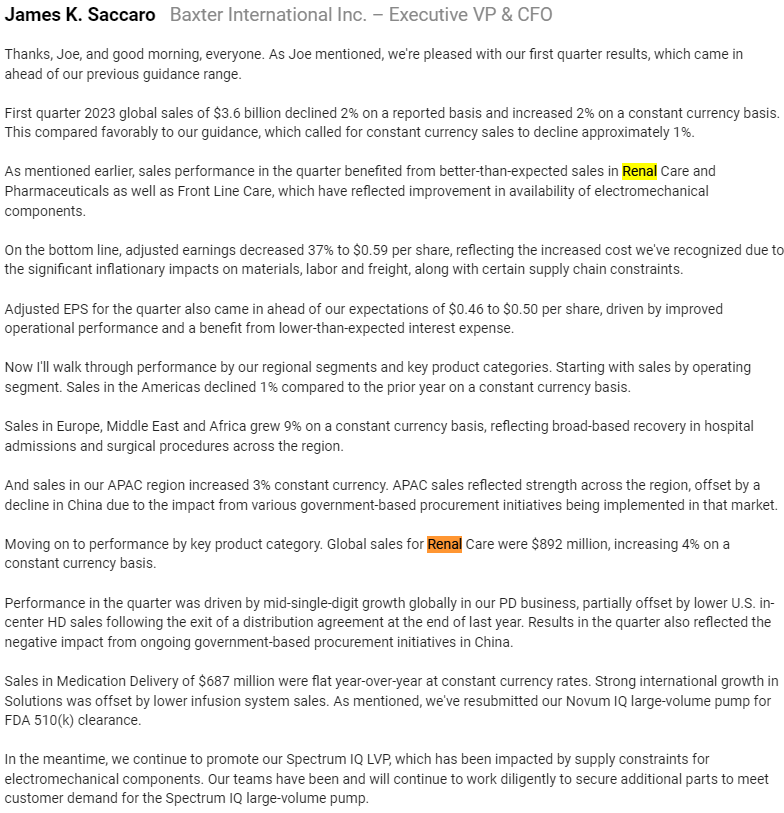

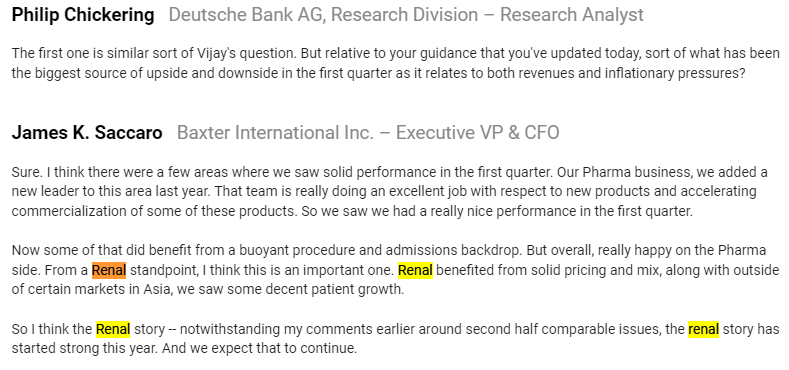

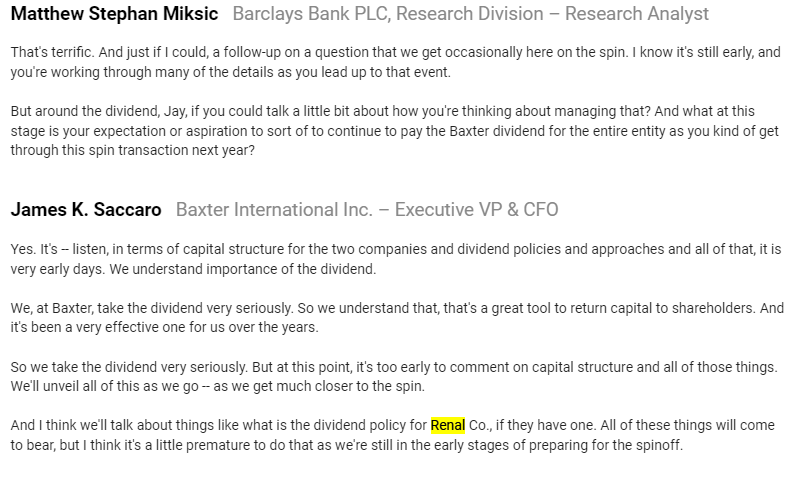

April 30, 2023 Update

This commentary is from Baxter’s April 2023 conference call:

January 19, 2023 Update

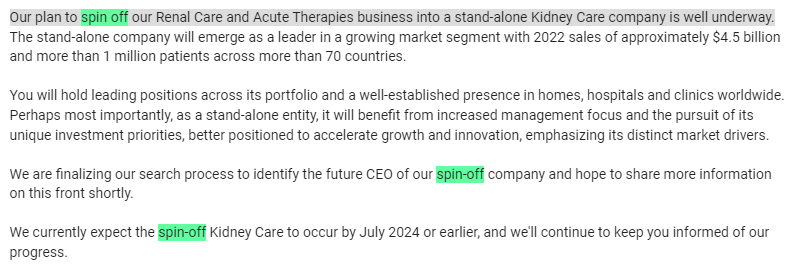

Baxter (BAX) announced on January 6 that it plans to spin off its Renal Care and Acute Therapies global business units into an independent publish company within 12-18 months. Here’s Baxter’s slide deck with additional details.

The spin-off generates revenue through peritoneal dialysis, hemodialysis, and acute therapies. It generated $4.7BN in sales in 2021. It will be viewed as a “badco” as its margins are lower than the corporate average and has a lower growth profile. Last year, Baxter had considered selling parts of its renal business as Bloomberg reported, but it appears that no attractive offers were made.

The RemainCo generated $10.9BN of sales in 2021. It’s key divisions are Pharmaceuticals, Medication Delivery, Front Line Care, Advanced Surgery, and Clinical Nutrition.

Baxter looks relatively cheap at 10.6x EBITDA and 11.5x forward EBITDA. Consensus calls for low single digit top line growth for the foreseeable future and ~10% EPS growth. Further, the company is relatively defensive. Nonetheless, the stock doesn’t look compelling to me, just modestly attractive.

From my perspective, this transaction doesn’t create any actionable opportunity today. Once the spin-off begins trading in 12-18 months, there could be an opportunity in the spin-off or RemainCo.

Leave A Comment