Mylan Spin-Off Quick Summary – January 31, 2020

Resources from Pfizer

Spin-off Slide Deck Presentation – July 29, 2019

Spin-off Press Release – July 29, 2019

Spin-off Webcast Replay – July 29, 2019

Investor Relations Contact Information

- Pfizer

- Chuck Triano, SVP of Investor Relations

- LinkedIn (no other contact info available)

- Mylan

- Melissa Trombetta, Head of Global Investor Relations

- Email: investorrelations@mylan.com

- Phone: (724) 514-1813

Other Resources

Pfizer-Mylan Generic Giant Solves Two Problems With One Deal – Bloomberg, July 29th, 2019

Pfizer Is Spinning Off Upjohn. What’s Left Will Be No Bargain – Barron’s, September 19th, 2019

Mylan’s Stock Soars After Merger Deal With Pfizer’s Upjohn – MarketWatch, July 29th, 2019

Understanding the Mylan-Upjohn Merger – SeekingAlpha, July 30th, 2019

Overview

On July 29, 2019, Pfizer and Mylan jointly announced that Pfizer’s Upjohn division would be combined with Mylan in a Reverse Morris Trust transaction. The transaction is expected to be tax-free for Pfizer shareholders, who will receive 57% of the shares of the new company, and taxable to Mylan shareholders, who will own 43% of the shares of the new company.

Why the Spin-off?

Both parties agreed to this transaction for a multitude of reasons that, in the end, should benefit both companies. For Pfizer, spinning off their off-brand and generics business in Upjohn should allow them to focus on their innovative core business, which is projected to grow faster than Upjohn, per analyst estimates. For Mylan, the key aspect of this deal was geographic revenue diversification. While Mylan has a strong foothold in the U.S. and Europe, Upjohn has a considerable presence in Asia and other emerging markets, allowing Mylan to reach an area of considerable growth without having to organically work to develop new markets on their own. This also diversifies Mylan revenues away from the U.S., which, considering the political climate surrounding drug pricing in America, should result in far lower volatility.

Spin-off Overview

Company

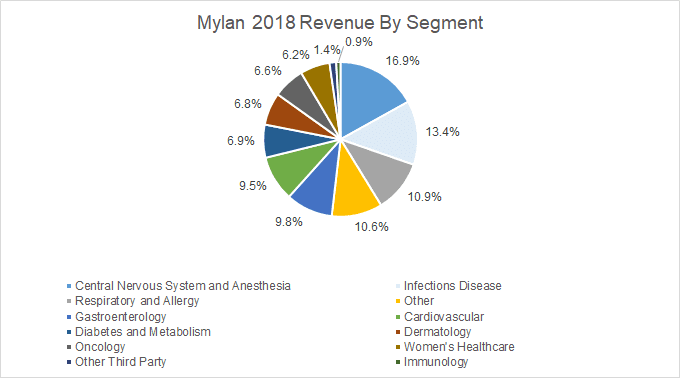

The new entity between Mylan and Upjohn will create substantial pure-play pharmaceutical company with revenue streams around the world. Mylan, as a stand-alone company, is a global generic and specialty pharmaceuticals company. For FY18, Mylan’s revenues included sales from drugs relating to Central Nervous System and Anesthesia, Infectious Diseases, Respiratory and Allergy, Gastroenterology, Diabetes and Metabolism, Dermatology, Oncology, Women’s Healthcare, Other, and Other Third party diseases.

Upjohn brings trusted, iconic brands, such as Lipitor (atorvastatin calcium), Celebrex (celecoxib) and Viagra (sildenafil), and proven commercialization capabilities, including leadership positions in China and other emerging markets.

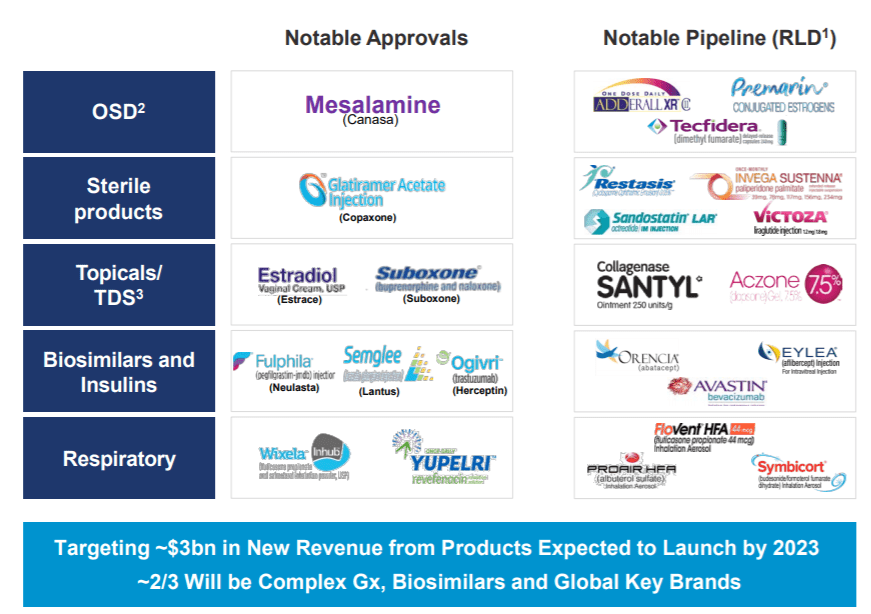

The pro-forma entity has grown relatively well in that past, essentially following along the secular trend of an explosion in generic pharmaceuticals, especially overseas. The pro-forma entity has been guided by management to grow modestly in the near term, with volume growth offset by pricing pressures. In the long term, management expects the company to drive long term growth through an accelerating pipeline of drugs. Currently, the pipeline for the combined entity contains ~10 newly approved drugs, with dozens more in various stages of the pipeline process. Management expected to recognize ~$3bn in revenues from these new drugs by 2023.

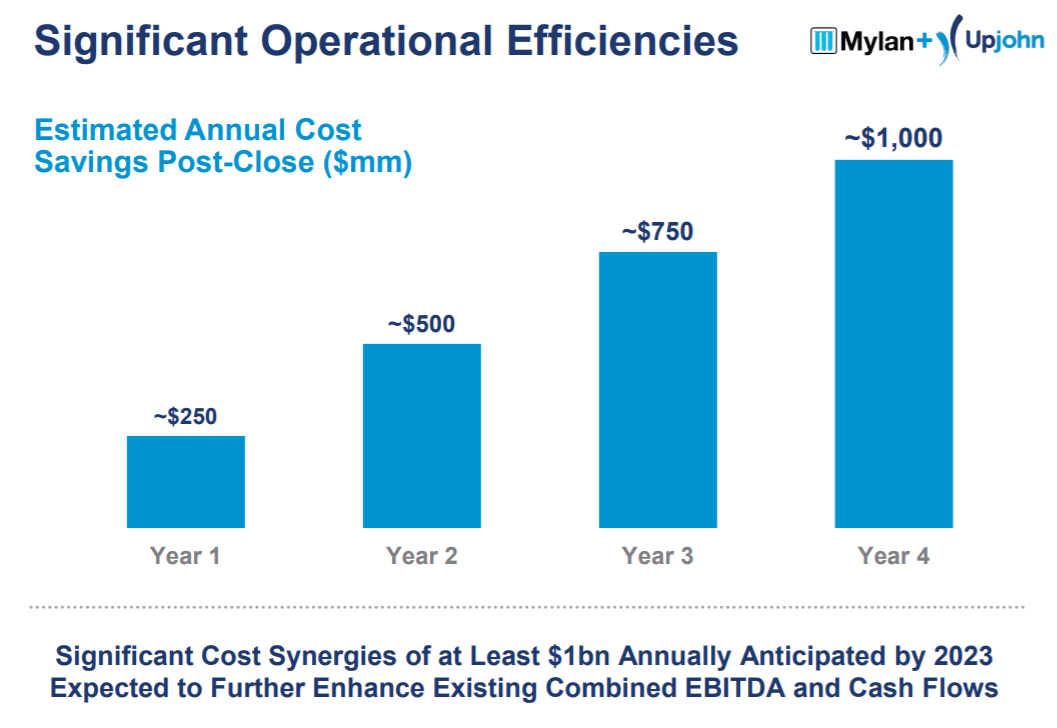

Although there have been secular pricing pressures in the pharmaceutical space, overall, this is a pretty good business. The pro-forma entity is expected to have EBITDA margins in the ~40% range, and cost synergies that accelerate from $250mm in the first year to $1bn in year four of the merger.

From a cyclicality perspective, the pharmaceutical industry will generally perform well in any economy. People have a fundamental need to keep themselves healthy, meaning they will pay almost any price in any economy for the drugs they need.

Industry

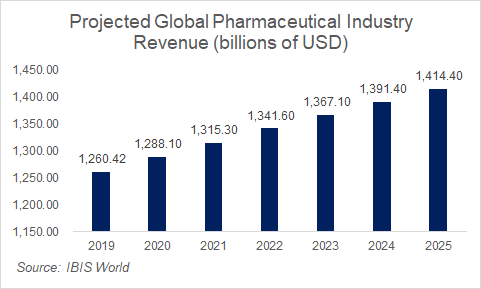

Consumer expenditures in the global pharmaceutical market are expected to grow modestly over the next few years, driven by an aging population and an increase in drug innovation. However, there are significant headwinds in the space as well, driven by cost cutting and price controls around both generic and patent-protected drugs. Growth will then have to come off of mostly volume, as price increases will be increasingly difficult to come by for these firms.

Competition

The newly formed Mylan-Upjohn entity will compete with pharmaceutical companies around the world. Some selections of comps, based on listed comps by both Mylan and Pfizer, include Lonzo, Perrigo, Endo, Ipsen, Mallinckrodt, and others. With the geographic scale that the new entity will create, however, investors should expect them to be a market leader very early on in their collaboration.

Customers

The merged company will essentially create, design, and manufacture pharmaceutical drugs, primarily distributing these drugs via wholesalers, then selling said drugs to pharmacies and hospitals, where they are prescribed to patients. Patients and their health insurers end up bearing the final cost of the drugs. A sample of Mylan and Pfizer’s largest customers indicates that they mostly sell to large name healthcare distributors, such as AmerisourceBergen, Cardinal Health, McKesson, and others.

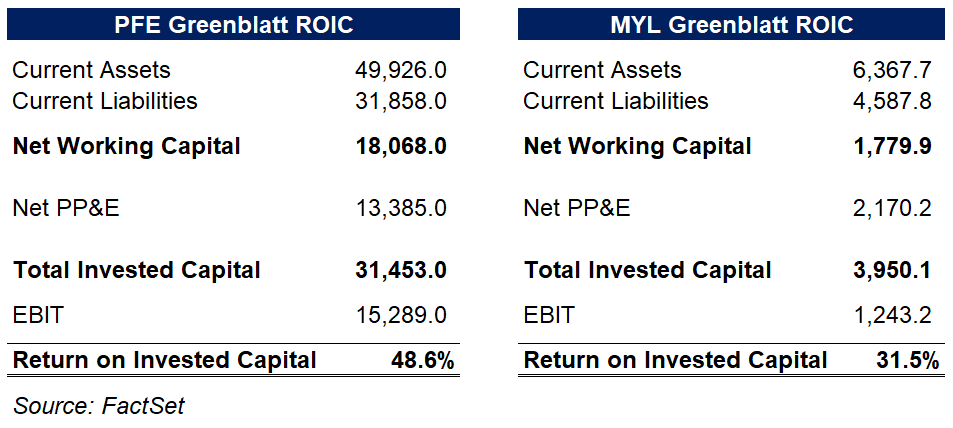

Quality of Business

Although the newly formed business is relatively high margin, which would traditionally be an indicator of a high-quality business, it does not come without its challenges. The business needs to continually pour money into aggressive research and development in order to develop new products.

These are relatively high ROIC companies, however, with the Greenblatt method of ROIC calculation giving PFE a 48.6% return on invested capital and a 31.5% ROIC for Mylan.

Capital Structure

Per PFE/MYL management, the spin-off will take on new debt of ~$24.5bn, of which ~$12bn will be earmarked as a cash closing payment from Upjohn to Pfizer. By management estimates of ~$7.5-8bn of EBITDA in the first year, leverage ratios will be around 3-4x EBITDA, depending on covenant levels, EBITDA adjustments, and cash levels. In the initial presentation regarding the transaction, it is clear that one of the main priorities for the new company will be expedited deleveraging, with a target of ≤2.50x by 2021. Additionally, the company clearly wants to return cash to shareholders as well, with a targeted divided payment of ≥25% of free cash flow, beginning in the first quarter after the transaction closes.

Investors have not yet been shown what an exact capital structure of the new entity will look like, but leverage ratios should be relatively manageable for a large company like this that will have clear access to capital markets at relatively attractive interest rates, in addition to a stable base of cash flows out of the business itself.

Management

New management for the combined entity has been announced, with major players being Robert Coury (Executive Chairman), Michael Goettler (CEO), and Rajiv Malik (President).

Robert Coury – Executive Chairman

Robert J. Coury is currently the Chairman of Mylan N.V. Under his leadership, Mylan has transformed from the third largest generics pharmaceutical company in the U.S. into one of the largest pharmaceutical companies in the world in terms of revenue, earning spots in both the S&P 500 and, prior to the company’s reincorporation outside of the U.S. in 2015, the Fortune 500.

Coury was first elected to Mylan’s board of directors in February 2002, having served since 1995 as a strategic advisor to the company. He became the board’s vice chairman shortly after his election and served as CEO from September 2002 until January 2012. Coury then served as executive chairman from 2012 until he became chairman in June 2016.

Since 2007, Coury has led Mylan through a series of transactions totaling approximately $25 billion, which transformed Mylan into a global powerhouse within the highly competitive pharmaceutical industry with a global workforce of approximately 35,000 that markets products in more than 165 countries and territories.

Michael Goettler – Chief Executive Officer

Michael Goettler is currently Executive Vice President, Pfizer and is a member of the Company’s Executive Leadership Team. In this role, he will be responsible for the newly created Established Medicines business, effective fiscal year 2019. With more than 23 years in the pharmaceutical industry, Michael has extensive commercial leadership experience and has lived and worked in multiple markets and regions, in both Asia/Pacific and Europe.

Michael joined Pfizer in 2009, as part of the Wyeth acquisition and has held a number of senior leader roles at both Wyeth and Pfizer with increasing responsibility across multiple therapeutic areas, including primary and specialty care. Most recently, he served as the Global President of Pfizer Inflammation & Immunology, leading Pfizer’s global five-billion-dollar portfolio of inline medicines, as well as late-stage, early development and research strategy and programs spanning rheumatology, dermatology and gastroenterology. Before then, he led Pfizer Rare Disease, where he initiated the company’s commercial move into gene therapy.

Prior to Wyeth, Michael held a variety of senior roles at Sanofi Aventis in the US and Japan in business development, eBusiness and global marketing.

Michael began his career working at Hoechst in Germany, where he quickly moved into roles of increasing responsibility, including Executive Vice President & CEO of Hoechst Marion Roussel Korea.

Michael, a native German, studied in Germany, France, and the U.S. He holds an M.B.A. from the University of Texas at Austin and graduated from the Koblenz School of Corporate Management in Germany. Prior to joining Pfizer, Michael worked at Hoechst, Aventis Pharma, and Sanofi.

Rajiv Malik – President

Rajiv Malik was elected to the board of directors of Mylan in 2013. He is a member of Mylan’s Science and Technology Committee.

Malik has served as Mylan’s president since Jan. 1, 2012, and has more than 36 years of experience in the pharmaceutical industry. Previously, Malik held various senior roles at Mylan, including executive vice president and chief operating officer from July 2009 to December 2012, and head of Global Technical Operations from January 2007 to July 2009. Malik has been integral in developing the strategies for the company’s acquisitions and, more importantly, in the execution and integration of acquisitions, specifically the generics business of Merck KGaA; the injectables business of Bioniche; Agila Specialties, a global injectables company; the EPD business; Famy Care’s women’s healthcare businesses; Meda, a leading international specialty pharmaceutical company that sells prescription and over-the-counter products; and most recently, the non-sterile, topicals-focused business of Renaissance Acquisition Holdings LLC.

Malik is responsible for the day-to-day operations of the company, which includes Commercial, Scientific Affairs, Manufacturing, Supply Chain and Quality. In his role, he also oversees Business Development and Information Technology. Malik has been instrumental in expanding and optimizing Mylan’s product portfolio, leveraging Mylan’s global research and development capabilities and expanding Mylan’s presence in emerging markets. Previously, he served as chief executive officer of Matrix Laboratories Limited (n/k/a Mylan Laboratories Limited) from July 2005 to June 2008. Prior to joining Matrix, he served as head of global development and registrations for Sandoz GmbH from September 2003 to July 2005. Prior to joining Sandoz GmbH, Malik was head of Global Regulatory Affairs and head of Pharma Research for Ranbaxy from October 1999 to September 2003.

Potential for Indiscriminate Selling

We do not expect heavy indiscriminate selling once the transaction is completed, as Mylan will be a large cap company. However, there is the possibility that PFE shareholders, who will own 53% of New Mylan, will sell their shares, creating modest selling pressure. On the other hand, there could be buying pressure as Mylan will pay a substantial dividend which will attract a whole new class of investors.

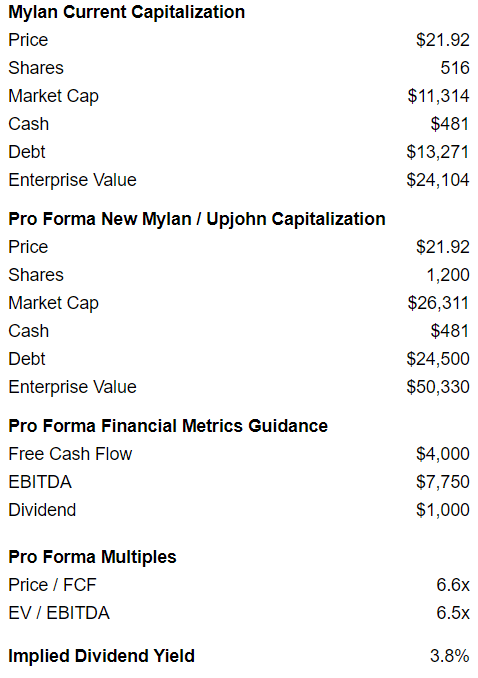

Valuation

On a pro forma basis adjusting for shares that will be issued to Pfizer shareholders, Mylan looks interesting, trading at 6.6x free cash flow and 6.5x EBITDA as shown below.

Mylan also plans to pay a dividend of at least 25% of free cash flow, implying a minimum dividend of $1BN and implied dividend yield of 3.8%.

This looks quite cheap.

Our Thoughts

We like the set up for Mylan. Shortly after the merger was announced, Mylan rallied but then fell as low as $17. If Mylan were to pull back to the mid to high teens, it would be an attractive buy. At that price, the implied yield on the stock would be close to 5%. Further, there would be significant additional free cash flow to de-lever and buy back stock.

Over the past couple of years, Mylan has been plagued by several controversies.

First, price fixing. There has been an ongoing lawsuit related to Teva, Mylan and other generic drug companies colluding to fix prices in order to diminish competition and maximize profits. This story summarizes the lawsuit well. From press reports, it appears the lawsuit has lost momentum. Further, if the lawsuit was successful, damages could not be too punitive or it would cripple the entire generics industry and harm patients (generics are generally significantly less expensive than branded medications). Healthcare focused investment bank Leerink Swan estimates that Mylan could face fines of $2.8BN for price fixing. New Mylan is going to generate at least $4BN of free cash flow and should have ample financial flexibility to pay any financial fine.

The second controversy relates to improper marketing of opioids. Here, Mylan is less exposed than many other pharma companies. Leerink Swan estimates that Mylan could ultimately have to pay a fine of $800MM. This would be a drop in the bucket for Mylan, especially after the merger with Upjohn.

It is telling that Pfizer was comfortable with the potential legal liability related to both price fixing and the improper marketing of opioids. After all, Pfizer shareholders will own 53% of new Mylan and so the long term viability of Mylan is important.

https://www.sec.gov/Archives/edgar/data/78003/000119312520018655/d877295d425.htm

Going to quote an exchange between analyst at Cowen and Pfizer mgmt from the above link:

“Stephen Michael Scala – Cowen and Company, LLC, Research Division – MD & Senior Research Analyst : I have a few questions. An increase in the dividend was mentioned twice, but it sounds as though Upjohn will be spun, not split, in which case the dividend will be reduced. So I’m wondering if you could clarify the dividend comment. And I assume the 2020 EPS guidance implies a spin, not a split. Secondly, on the abrocitinib versus Dupixent study, given the fact that it is completed, Mikael, I’m wondering if the data met the very positive portrayal you provided on the Q3 call, which included superior itch relief to Dupixent. And then lastly, will the proof-of-concept DMD data be presented at the March 31 meeting?

Albert Bourla – Pfizer Inc. – Chairman of the Board & CEO : No, thank you very much, Steve. Very good questions. So Frank, why don’t you clarify once more the dividend?

Frank A. D’Amelio – Pfizer Inc. – CFO & EVP of Global Supply & Business Operations : Sure. So Steve, in terms of the guidance, you’re right. It assumes a spin, not a split. And then in terms of the dividend, you said — I think you said in your question it’d be a reduction. I don’t see it that way. What we’ve said is the sum of Viatris dividend and our dividend would equal the current dividend that a Pfizer shareholder receives today. So I don’t see a reduction in the dividend. The dividend income will be kept whole. And I think we’ve been very clear about that all along.

Frank A. D’Amelio – Pfizer Inc. – CFO & EVP of Global Supply & Business Operations : Right. And Steve, I can quickly run the numbers for you if you’d like. Just — so if you think what Viatris has said is their first full year of about $4 billion of free cash flow, they pay about 25% of that in the dividend, so that’s $1 billion. Total Viatris will have about 1.2 billion shares. You put the $1 billion over 1.2 billion shares, it’s about $0.83. The exchange ratio is about .12. You put 100 shares of Pfizer, you get 12 shares of Viatris. Assuming a spin, that’s roughly $10 a share. We would reduce our dividend on an annual basis by that $10. But the sum of our dividend plus that $10…

Albert Bourla – Pfizer Inc. – Chairman of the Board & CEO : $0.10.

Frank A. D’Amelio – Pfizer Inc. – CFO & EVP of Global Supply & Business Operations : $0.10, I’m sorry, thank you, would equal the — what a Pfizer shareholder gets today. And in my thing, it’s $10.

Albert Bourla – Pfizer Inc. – Chairman of the Board & CEO : Yes.

Frank A. D’Amelio – Pfizer Inc. – CFO & EVP of Global Supply & Business Operations : $10, not $0.10.

Albert Bourla – Pfizer Inc. – Chairman of the Board & CEO : Thank you very much to both of them. By the way, Frank, as always, was right. It’s $10 for 12 shares for Mylan. So…”

Okay, so the way I take that, is $10 per 100 shares of Pfizer will be removed from Pfizer’s dividend. Pfizer is paying $1.52 / share currently, so 100 shares pays $152, currently. To keep the dividend income “the same,” investors will have to keep both, but Pfizer pays out about $8B per year in dividends ($1.992B in most recent Q) and the executive is suggesting they’ll reduce that to ~$7B. Since Pfizer is keeping its dividend pretty high (~ $1.33 / sh ?) I expect Pfizer shareholders to sell Viatris (the new company after merging with Mylan) especially if there are not emphatically clear statements made by Viatris about their dividend?

I’ve seen too many spinoffs with declining sales and high leverage decline significantly. I would not buy VTRS unless it is below $12. I am bullish on PFE, It is now a highly focused company selling at reasonable multiples with forecasted 5% annual revenue growth and 10% profit growth for the next 5 years. I believe it is undervalued.

Interesting on PFE. It does look quite reasonable. With regards to VTRS, I agree debt + declining sales is not a good combo. With VTRS, I’m comfortable with it for the following reasons. 1) Net to EBITDA is 3.1x. This doesn’t seem aggressive. Further, they will generate $4BN of free cash flow and can aggressively pay down debt/buy back stock. 2) The expected dividend at current VTRS’ current price works out to a 4.8% yield. It’s quite juicy and will be a hard catalyst to rerate shares. I see it playing out similarly to how KTB rallied fairly quickly after initial indiscriminate selling. I think the rally was largely driven by the dividend.