BBX Capital: A Dollar Selling for 30 Cents

December 28, 2020

Ticker: BBXIA

Market Cap: $94MM

Enterprise Value: $40MM

Price: $4.85

Fair Value: $7.50

Upside: 55%

Background

While I closely follow all stock spin-offs, I’m especially drawn to the tiny ones. They are too small for institutional investors (and most retail investors), and sometimes I find some incredible opportunities.

You will find a lot of crap in the micro-cap spin-off land but every so often you find a Liberated Syndication (LSYN) which makes it all worthwhile.

Back in June 2020, BBX Capital announced that it would spin-off all non-Bluegreen related businesses into a new public company, New BBX Capital.

At the time of the spin-off announcement, BBX capital owned the following assets:

- 93% of Bluegreen Vacation Corp (BXG), a public timeshare company

- BBX Capital Real Estate LLC, which owns various real estate properties and joint venture investments

- BBX Sweet Holdings, LLC, which owns various businesses in the confectionary (candy) industry

- Renin Holdings, LLC, is one business that manufactures sliding doors and other home products

The spin-off took place on October 1, 2020, and trades under the ticker BBXIA.

The remaining company changed its name to Bluegreen Vacation Holding Company (BVH) as it’s only asset (besides cash and debt) is its 93% ownership stake in Bluegreen Vacation (BXG).

Before the spin-off started trading, I was vaguely interested in the set up, but didn’t initially spend too much time due to corporate governance concerns (we will discuss those later).

But after seeing where the spin-off started to trade, I dropped everything and dug into it.

It was clear the stock was trading at a small fraction of any reasonable estimate of fair value, even assuming a large discount for corporate governance concerns.

While the stock has appreciated since the time of the spin-off, it is still only trading at 30% of book value ($16.24), an unsustainably low valuation, given book value consists primarily of real estate and cash.

The Assets

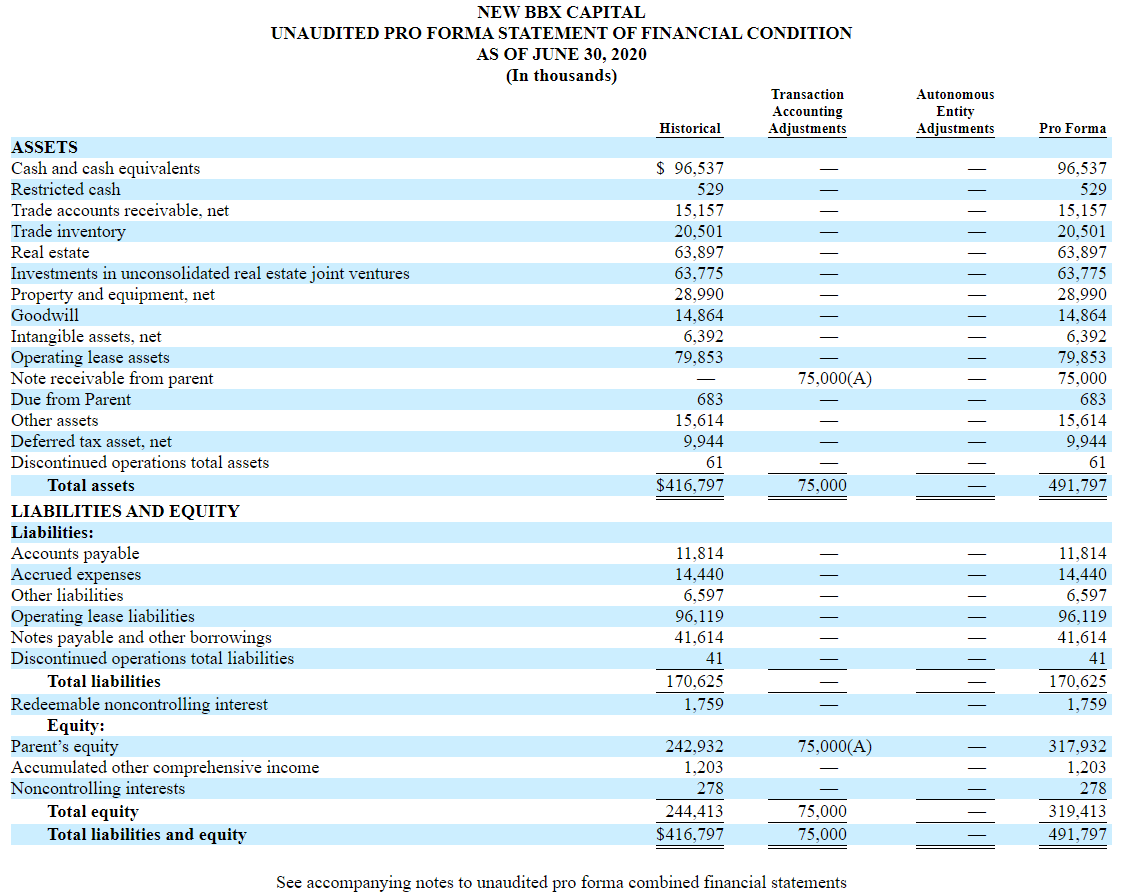

As disclosed in the spin-off’s Information Statement, New BXX Capital has a strong balance sheet as shown below.

If we just consider cash and cash equivalents ($96.537MM) and other borrowings ($41.614MM), we can see that the company has net cash of $54.9MM. At its current price, BBX Capital has a market cap of $94.3MM (19.276MM shares outstanding). Thus, the company has over half its market cap in net cash. BBX Capital did use $5MM of its cash to help fund the recent acquisition of Colonial Elegance (discussed below).

The next most important asset to consider is a $75MM note receivable from its parent company, Bluegreen Vacation Holding Company (BVH). This note pays 6% interest per year and is due in 5 years.

Bluegreen Vacation Holding Company is reliant on dividend payments from Bluegreen Vacation. If Bluegreen Vacation goes bankrupt, New BBX Capital would not be able to collect its $75MM note receivable. While anything is possible, Bluegreen Vacation generated $46.1MM in free cash flow in the first nine months of 2020 despite the pandemic. In normal times, Bluegreen Vacation is an incredibly cash generative business. In the past five years, Bluegreen has paid out $257MM in dividends (it currently has a $382MM market cap).

In other words, I view the $75MM note payable as money good.

Besides cash and the note receivable, New BBX Capital has three businesses:

BBX Capital Real Estate LLC

BBX Real Estate acquires, develops, constructs and manages real estate.

BBX Capital originally got into the real estate business after it sold its banking business to BB&T Corporation in 2012, but retained certain real estate assets and non-performing loans that it worked out.

In addition, BBX Capital Real Estate owns a 50% equity interest in The Altman Companies, a developer and manager of multifamily apartment communities. BBX Capital Real Estate had total assets of $161.9 million as of June 30, 2020.

BBX Sweet Holdings, LLC

BBX Capital has acquired many companies in the confectionery (candy) industry, including IT’SUGAR, Hoffman’s Chocolates, and Las Olas Confections and Snacks. IT’SUGAR is a specialty candy retailer which operates in retail locations throughout the United States. Its products include bulk candy, candy in giant packaging, and novelty items that are sold at its retail locations, which include a mix of high-traffic resort and entertainment, lifestyle, mall/outlet, and urban locations across the United States.

Hoffman’s Chocolates is a retailer of gourmet chocolates with retail locations in South Florida. Las Olas Confections and Snacks is a manufacturer and wholesaler of chocolates and other confectionery products.

BBX Sweet Holdings had total assets of $133.2 million as of June 30, 2020.

It was recently disclosed that IT’SUGAR has filed for bankruptcy reorganization due to the pandemic. Thus, I’m assuming that the entire confectionary division is worth $0. This is probably conservative.

Renin Holdings, LLC

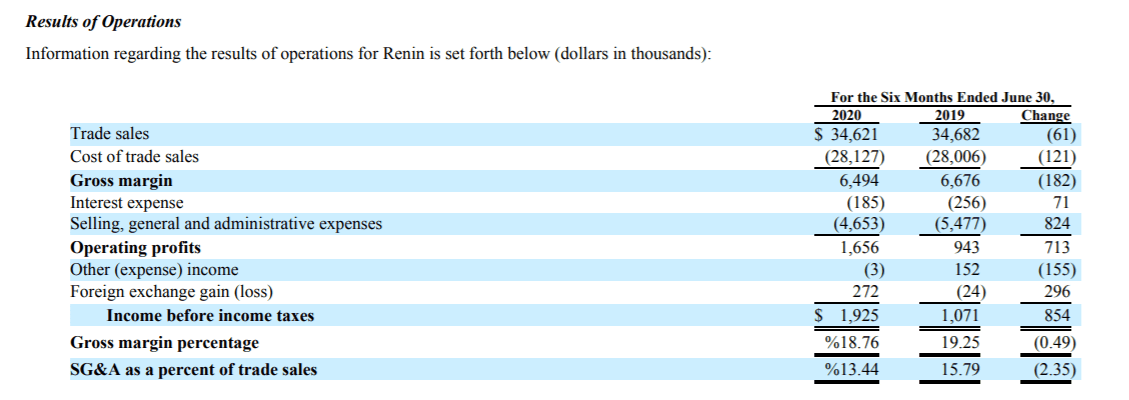

Renin is engaged in the design, manufacture, and distribution of sliding doors, door systems and hardware, and home décor products and operates through its headquarters in Canada and two manufacturing and distribution facilities in the United States and Canada. Renin had total assets of $35.9 million as of June 30, 2020.

In 2020, Renin’s profitability has spiked due to lower spend on travel and trade show costs.

I assume Renin is worth $14.4MM (8x 2019 EBIT of $1.8MM).

Renin recently acquired Colonial Elegance, a supplier and distributor of building products, including barn doors, closet doors, and stair parts. This purchase complements its existing sliding doors, door systems and hardware business. Renin paid $39MM for the acquisition but that price includes $5.1MM of excess working capital. As a result, the purchase price goes down to $33.99MM. EBITDA in the past year was $8.1MM CAD, or $6.1MM USD. As such, the purchase price was 5.6x EBITDA, which seems rather cheap.

The acquisition was funded by a $5MM contribution from BBX Capital and a credit facility that was associated with the acquisition.

What’s it Worth

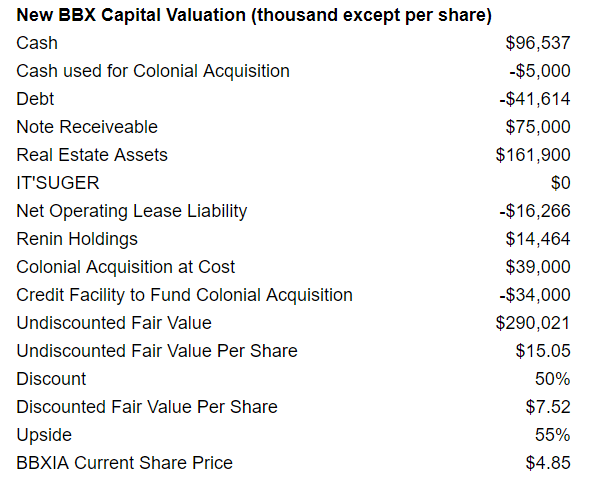

New BBX also has operating lease assets and liabilities that net to an operating lease liability of $16.2MM. I will subtract this from my fair value estimate.

If you add it all up, you get an asset value of $15.05 per share versus BBXIA’s current share price of $4.85.

Even if you apply a 50% discount to the company’s asset value, you still reach a fair value of $7.52.

Will This Business Generate or Consume Cash Going Forward?

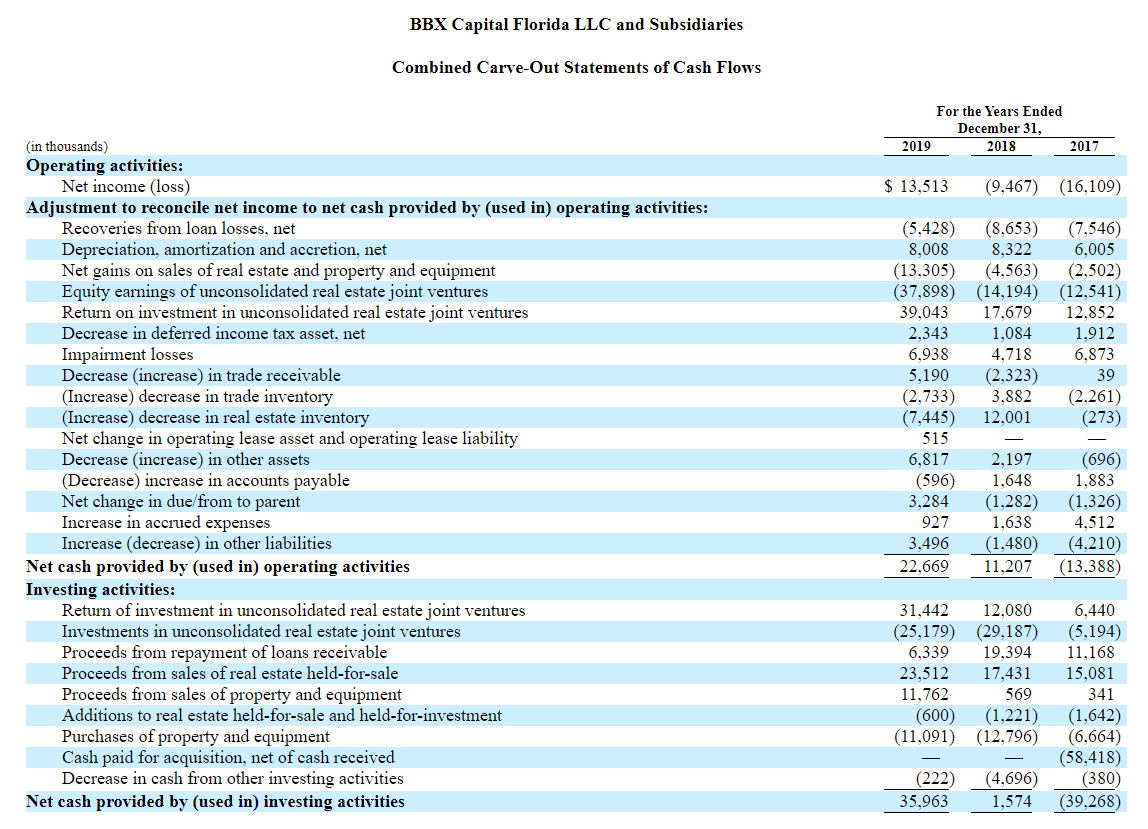

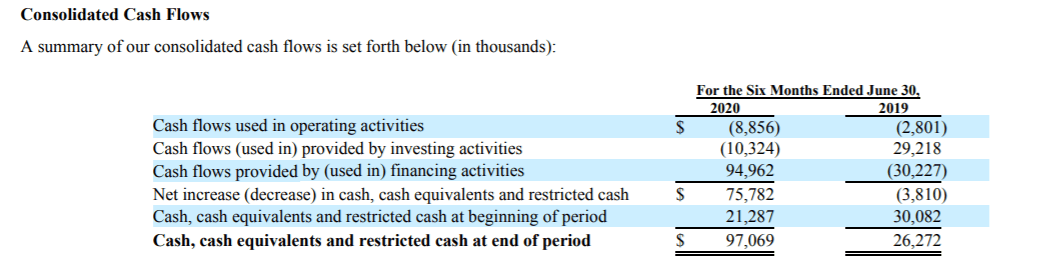

In 2018 and 2019, New BBX Capital generated positive free cash flow as shown below. Further, historically real estate activity has been a net generator of cash.

Through the first 6 months of 2020, New BBX Capital has consumed ~$19MM of free cash flow (as shown below), but in a normalized environment, New BBX Capital should generate cash or at least be breakeven.

Why Does This Opportunity Exist?

First, it’s a spin-off. Oftentimes, dislocations are associated with spin-offs. Especially with micro-cap spin-offs.

Second, corporate governance issues.

Initially, I didn’t spend much time on this spin-off because corporate governance left a bad taste in my mouth.

In the Information Statement for the spin-off, it reads:

As described in further detail in the Information Statement, in contemplation of the Spin-Off, the Parent’s Compensation Committee approved the acceleration of vesting of all unvested restricted stock awards that were previously granted by the Parent, all of which were held by the Parent’s executive officers. In connection with such vesting acceleration, the Parent will recognize compensation expense during the quarter ending September 30, 2020 of approximately $19.8 million (which represents the unrecognized compensation expenses associated with the restricted stock awards as of June 30, 2020). In addition, the Parent’s Compensation Committee approved the payment, prior to the consummation of the Spin-Off, of a total of approximately $19.5 million in cash to the Parent’s executives for 2020 services and the payout of cash to settle the Parent’s long-term incentive program for 2020 (which, in previous years, was generally paid primarily in stock awards).

This looks pretty egregious to me.

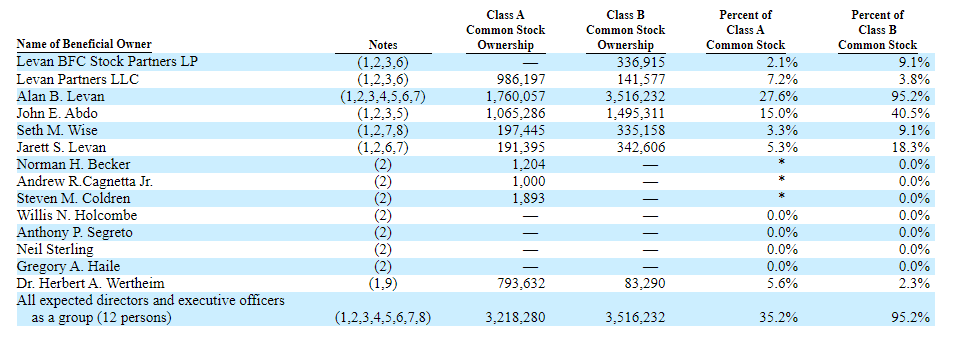

As shown below, Alan Levin controls the stock based on his class B share ownership and basically dictates executive compensation.

However, New BBX Capital is trading at such a discount to any reasonable estimate of fair value, that I’m willing to hold my nose and buy the stock.

Further, the Levin family owns 42.2% of the common stock, and as such, is incentivized to increase value at the company. Also, the BBX Capital team strikes me as relatively savvy capital allocators. The company sold BankAtlantic Bancorp, Inc to BB&T in 2012, but retained certain real estate which it was able to monetize effectively.

This article explains how they took advantage of weakness in Bluegreen Vacation to acquire shares in the company and ultimately take it private before taking the company public again.

Further, BBX Capital has already announced a $10MM share repurchase which represents 11% of the company’s market cap. Why buy back stock unless you care about shareholder value?

My best guess is that the Levin family takes this company private (steals the company) at a discount to its book value but at a significant premium to where the stock is currently trading.

The other important thing to note is that this was a taxable spin-off. Thus, the company can be sold at any time (tax free spin-offs cannot be sold for two years).

Conclusion

While corporate governance and executive compensation issues at New BBX Capital are concerning, the stock is trading at a completely dislocated price relative to the value of the company’s assets. It’s hard to estimate exactly what the stock is worth, but I think ~$7.50 (50% discount to asset value) is a reasonable estimate.

Risks

- Real estate value is overestimated.

- I’m not a real estate expert, it’s difficult to estimate the company’s real estate value with precision. However, the company has historically generated significant proceeds from its real estate activities. Further, one can discount my real estate fair value estimate by 50% or more and the stock still looks attractive.

- Value is destroyed by poor acquisitions.

- While the company’s acquisitions in the confectionery industry have not worked out, it has been successful in the real estate industry and with its Bluegreen Vacations investment.

- Continued poor corporate governance.

- Unfortunately, I think this is likely to continue. Nonetheless, this risk is well established, and the stock’s current price reflects it fully.

Other Resources

Disclosure

Rich Howe, owner of Stock Spin-off Investing (“SSOI”), is long BBXIA. All expressions of opinion are subject to change without notice. This article is provided for informational purposes. Please do your own due diligence and consult with an investment adviser before buying or selling any stock mentioned on www.stockspinoffinvesting.com.

Very well written and simply to understand investment thesis. Two comments from my side: 1. You can argue that the 50% discount could be deducted only from the real estate and Renin assets and not from the note and the cash, this would make the intrinsic value higher, 2. Cash burn, will the business be cash flow positive in 2021 or at least break even?

I agree that it doesn’t make sense to discount the cash and note receivable, but I’m doing it just to be extremely conservative.

Thanks for sharing! I must say, I was at the It’s Sugar retail location in the American Dream mall just last week and it’s really amazing. Not sure how that plays in to the $0 equity value you attributed to it as I’m not privy to any of the bankruptcy filings.

That’s great to hear! Yes I’m ascribing zero value to It’Sugar, but I think there could be upside.

Thanks for the writeup – the Clark writeup makes the point that exec comp @ $20MM per year is a liability of say $150MM which more or less erodes the discount to book value. What do you think?

It’s a fair point. My thought is that it deserves to trade at a discount to book value but not a 70% discount given that book value consists of cash, a note receivable that I believe is “money good”, and valuable appreciating real estate which is mainly in Florida (benefitting from people leaving high tax states). What is the right discount to book value? I don’t know, but 50% seems reasonable which implies that the the stock is worth $7.50. The other thing that gives me comfort is the Levin family owns ~42% of the common stock. So at the end of the day, they are aligned with minority shareholders. That family could make a lot of money by taking the company private at a premium to its current price but at a discount to book value. Ultimately, that’s what I think happens.