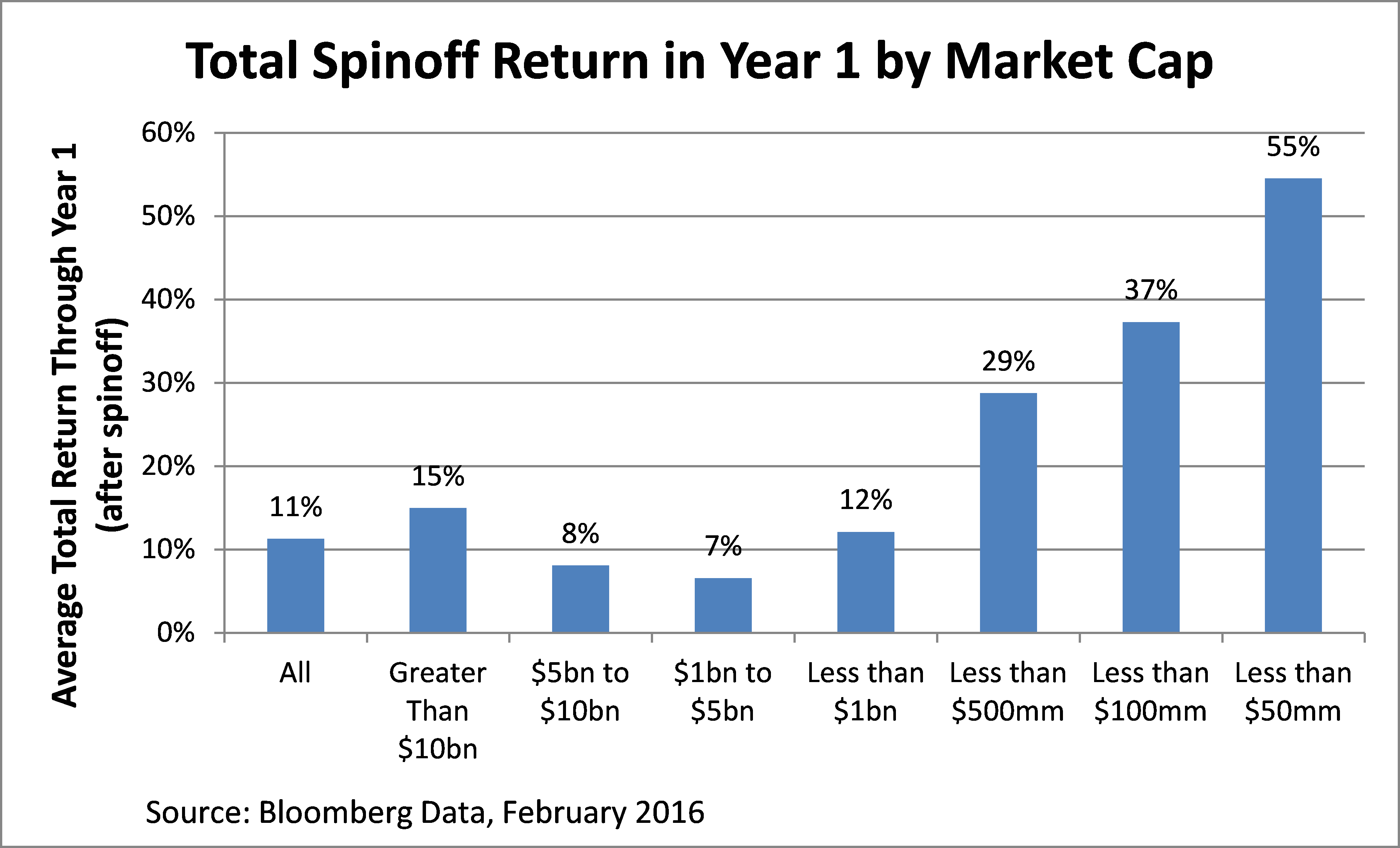

Nuvectra (Ticker: NVTR) first piqued my interest because it is a microcap spinoff and microcap spinoffs generate huge returns in year one. See the chart below:

However, you have to be extremely careful investing in spinoffs and especially microcap spinoffs. While the average performance is extremely attractive, there is huge dispersion in returns. As an example, the average return for spinoffs with less than a $500mm market cap is +29% in the first year of trading. But the median return is only +7%. The outliers skew the results.

Similarly, a recent Deloitte and Edge Group Study found that top quartile performing spinoffs generate +98% total return in their first year while bottom quartile spinoffs generate 1 year returns of –39%.

So just to reemphasize, you need to be very careful.

Getting Back to Nuvectra

A couple weeks ago, I got an email from the folks at www.stockspinoffs.com telling me that Nuvectra was trading below its cash levels. The stock ended up bottoming at about $4.30 which translates to a market cap of ~$44mm. The company was spun off with $67.6mm of net cash. This got my attention.

After doing a bunch of work, I’ve concluded that I don’t know how much NVTR is worth, but I think it’s worth a lot more than $6.87 (its current trading price).

Let me explain…

What is Nuvectra?

Nuvectra is a med tech company. It used to be a division of Greatbatch (Ticker: GB) which is an outsourced med tech manufacturing company. At the time of the spinoff announcement, Greatbatch had just announced a big acquisition and it decided to spinoff NVTR (formerly known as QiG Group) as the division had matured but was non-core and wasn’t getting properly valued as a small division within a $1.7bn (at the time) market cap company.

How does Nuvectra make money?

Well it doesn’t yet and it won’t for the foreseeable future….but it should generate a lot of revenue

Nuvectra’s First Product: Algovita

Nuvectra has two products currently. The first product is called Algovita. It is approved for the $1.6bn spinal cord stimulation (SCS) market for chronic pain. It is also expected to be approved for the $500mm sacral nerve stimulation (SCS) market for bladder and bowel control.

What exactly is the Algovita Spinal Cord Stimulation System?

It is an implantable device which delivers steady pulses of energy to certain nerves in and around the spinal cord in order to dull or mask severe pain.

Here’s the Mayo Clinic’s definition for Spinal Cord Stimulation:

“A small wire carries the current from a pulse generator to the nerve fibers of the spinal cord. When turned on, the stimulation feels like a mild tingling in the area where pain is felt. Your pain is reduced because the electrical current interrupts the pain signal from reaching your brain.”

Here’s a great video (~3 minutes) that explains how spinal cord stimulation works to relieve pain:

https://treatingpain.com/treatment/spinal-cord-stimulation

As mentioned earlier, the spinal cord stimulation market for chronic pain is currently a $1.6bn market. The market is currently made up of four major players: Boston Scientific, St. Jude Medical, Medtronic, and Nevro (newer player).

The neuromodulation platform that was developed at Greatbatch and is now Nuvectra was developed by the technology innovation group within Greatbatch after carefully working with patients and physicians to understand key areas of need. This group has been working since 2009 to develop differentiated products. The product is finally ready and FDA approved.

Key Differentiating Factors for Algovita vs. the Competition

- No more paresthesia. Traditional spinal cord stimulation is associated with paresthesia (a tingling sensation) which many patients don’t like. Algovita delivers higher frequency outputs than most other products on the market. As a result, Algovita doesn’t cause paresthesia.

- Thinner lead. The lead (the wire that carries the pulse) is thin and flexible, which is an improvement over the products that are currently on the market. This is important for several reasons. First, it makes it easier for the physician to place the stimulators in a region that will best block the pain. It’s also important because it reduces risk of migration (the lead and/or stimulator moving) and breakage of the lead.

- Intuitive interface. The wireless interface (for the physician and patient) is very intuitive and user friendly. It helps with programing and user control. It’s easier to use than other spinal cord stimulation systems.

How Much Revenue will Algovita Generate?

Piper Jaffrey is the only sell side firm that currently covers Nuvectra. Piper Jaffray estimates Algovita will generate revenue of $29.7mm, $55.1mm, $88.9mm, and $108.7mm in Fiscal 2017, 2018, 2019, and 2020, respectively.

The spinal cord stimulation market is $1.6bn in size and is growing at 6% per year. Assume the market grows to $2bn by 2020, Piper Jaffray’s estimate of $108.7mm in sales in 2020 represents only 5.4% of the market. In Nuvectra’s Form 10, Nuvectra management reviews key assumptions that are used in order to test for whether goodwill is impaired. One of management’s assumptions is that Nuvectra market share grows from low single digits in the early years to a maximum of 6% to 15%. As such, Piper Jaffray’s estimates seem reasonable, especially given that Nuvectra has worked on this project for over seven years in close consultation with patients and spinal cord stimulation physician thought leaders.

Nuvectra’s Second Product: PelviStim

Nuvectra’s second product is called PelviStim. The product is focused on sacral nerve stimulation for bladder and bowel control. The sacral nerve stimulation market is currently ~$500mm, growing at 10% per year, and dominated 100% by Medtronic. The market has seen limited innovation over the past decade so it could be a great opportunity for Nuvectra.

Similar to spinal cord stimulation, sacral nerve stimulation works by sending a mild pulse through a lead (wire) to the sacral nerve (important nerve for bladder control). The theory is that mild stimulation of the sacral nerve helps the nervous system and brain coordinate and function properly, allowing patients to have better bladder and bowel control.

Here’s a 3 minute video that explains how sacral nerve stimulation works:

https://www.youtube.com/watch?v=ONaa8d96m8Q

Management expects to launch PelviStim in early 2018. Piper Jaffray notes: “While details of the PelviStim SNS system have not been made public, we expect a similarly (in reference to Algovita) differentiated technology offering vs. currently available commercial technologies.”

How Much Revenue can we Expect from Pelvistim?

Piper Jaffray models sales ramping up to $56mm by 2020. Assuming the market grows to $750mm by 2020 (market is growing by about 10% per year), Piper Jaffray’s estimate implies 7.5% market share and seems reasonable.

Other Revenue

Nuvectra has a couple of other products in development, but I’m not going to spend any time on them as they are of lower importance.

Implicit Guidance?

In the Piper Jaffray initiation report, the analyst wrote (italic and underline added by me):

“On an enterprise-wide basis, we are modeling FY16E revenue of $13.6mm, which represents 160% growth of FY15. In FY17 and FY18, we model revenues of $35.1mm (+158%) and $78.3mm (+123%), respectively. Management believes it can achieve these targets via continued investment in building out Nuvectra’s domestic field force and partnering with OUS distributors.”

To me the phrase “management believes” implies management guidance. Management has not hosted any conference calls or issued any sort of guidance, but the analyst from Piper Jaffray has spent significant time with management as Piper was Greatbatch’s financial advisor during the spinoff and acted as sole lead arranger on the Nuvectra credit facility.

Management and Executive Compensation

Piper Jaffray notes in its report:

“An important point for investors should be the management team of Nuvectra. This is an experienced ‘been there, done that’ group with deep expertise in the neuromodulation industry with CEO Scott Drees and Global Sales & Marketing head Tom Hickman having come from Advanced Neuromodulation Systems (formerly ANSI) which was acquired by St. Jude in 2005 for $1.3bn. Additionally, NVTR’s headquarters are in Plano, Texas, the same area in which STJ’s neuromodulation franchise is based. While it is an inherently difficult attribute to quantify, we note that the majority of implantable neuromodulation physicians and industry players are a relatively tight knit group and that relationships can play a key role in driving commercial therapy adoption.”

I just wanted to re-emphasize CEO Scott Drees’ pedigree. He has 34 years of experience in the medical devices industry. He was formerly President and Executive Vice President, Worldwide Sales and Marketing, at Advanced Neuromodulation Systems, a neuromodulation company that was acquired by St. Jude for $1.3bn. For the past seven years, he’s been President and CEO of Neuromodulation Ventures, LLC, an incubatory for novel neuromodulation companies. This dude is a neuromodulation PRO.

In sum, this is a very strong management team. I don’t think they believe NVTR will remain a microcap stock for long. The plan as I see it is to eventually sell to one of the big guys (MDT, BSX, or STJ). The deal would be extremely accretive as the acquirer would acquire the revenue of NVTR but eliminate almost all of the costs (they would all be redundant) associated with Nuvectra.

Executive Compensation

In his “special situations” investing book You Can Be a Stock Market Genius, Joel Greenblatt writes:

“Insider participation is one of the key areas to look for when picking and choosing between spinoffs – for me, the most important area. Are the managers of the new spinoff incentivized along the same lines as shareholders? Will they receive a large part of their potential compensation in stock, restricted stock, or options?”

So Joel Greenblatt, the king of spinoff investing, thinks that insider participation is the most important factor when choosing between spinoffs.

Let’s take a look at Nuvectra’s executive compensation and insider participation…

Scott Drees (CEO) will make a $400,000 salary in 2016, while Walter Berger (CFO), will make $350,000. While this is a lot of money, it pales in comparison to what other CEOs and CFOs are pulling in. To add context, Glassdoor.com just found that the average S&P 500 CEO makes $13.8mm per year in total compensation. In that light, Nuvectra’s executive compensation actually seems very reasonable.

The Form 10 states that Scott Drees (CEO) and Walter Berger (CFO) will each own at least 2% and 1%, respectively, of the number of shares of Nuvectra common stock outstanding immediately following the completion of the spin-off. So at a bare minimum, the CEO currently owns 2% of NVTR stock which translates to a value of about ~$1.4mm. As such, the performance of the stock has a much bigger impact on his net worth than his salary. This is good news for investors. He is incentivized to act like an owner.

I also found an interesting side note when reading through the executive compensation portion of the Form 10:

“It is currently intended that this one-time equity award grant will be in lieu of Mr. Drees’ (CEO) participation in any equity incentive plan established by Nuvectra for the three-year period following the completion of the spin-off.”

Separately:

“It is currently intended that this one-time equity award grant will be in lieu of Mr. Berger’s (CFO) participation in any equity incentive plan established by Nuvectra for the three-year period following the completion of the spin-off.”

I read this to mean the CEO and CFO have both elected to front load their stock options, implying that they believed that the stock would be undervalued shortly after the spinoff when their stock options are priced. Perhaps, I’m seeing something that’s not there, but that’s my take.

Another factor I looked into was total equity compensation (stock options, restricted stock, etc.). Reading the Form 10, I learned that 1,128,410 additional shares are reserved for equity compensation. This translates to ~11% of shares outstanding. Additionally, on January 1 of each year for nine years, the amount of shares eligible for equity compensation increased by 4% of shares outstanding. This is huge. So on January 1, 2017, the amount of shares eligible for equity compensation goes from 11% of shares outstanding to 15% of shares outstanding. On January 1, 2018, the amount increases from 15% to 19% and so on.

What does this mean? If Nuvectra does well or gets acquired, the management team is going to become rich (or richer). And so will investors. While some investors will look at this negatively (due to potential dilution), I view this as a strong positive. Up until I read this section of the Form 10, I had wondered why CEO Scott Drees would take the job. He (as Head of Sales for ANS) already sold a $1bn+ business to STJ. For the past five years, he’s been running his own neuromodulation consulting firm. Why join Nuvectra? Because now he (as CEO) has the opportunity to build another large neuromodulation company and hopefully sell it for a $1bn+ to STJ (or BSX or MDT).

Classic Spinoff Dynamics at Play

To me, Nuvectra represents a classic spinoff situation.

Here’s Joel Greenblatt from You Can Be a Stock Market Genius, to describe what a classic spinoff situation is:

“Generally, the new spinoff stock isn’t sold, it’s given to shareholders who, for the most part, were investing in the parent company’s business. Therefore, once the spinoff’s shares are distributed to the parent company’s shareholders, they are typically sold immediately without regard to price or fundamental value.

The initial excess supply has a predictable effect on the spinoff stock’s price: it is usually depressed. Supposedly shrewd institutional investors also join in the selling. Most of the time spinoff companies are much smaller than the parent company. A spinoff may be only 10 or 20 percent the size of the parent. Even if a pension or mutual fund took the time to analyze the spinoff’s business, often the size of these companies is too small for an institutional portfolio, which only contains companies with much larger market capitalizations.

Many funds can only own shares of companies that are included in the Standard & Poor’s 500 Index, an index that includes only the country’s largest companies. If an S&P 500 company spins off a division, you can be pretty sure that right out of the box that division will be the subject of a huge amount of indiscriminate selling. Does this practice seem foolish? Yes. Understandable? Sort of. Is it an opportunity for you to pick up some low-price shares? Definitely.”

This is exactly what happened with Nuvectra. Nuvectra’s parent company Greatbatch has a market capitalization of over $1bn. It is an outsourced manufacturer of medical devices. On March 14th, investors in Greatbatch discovered in their accounts shares of Nuvectra, a $100mm market capitalization (at the time of the spinoff), early-stage neuromodulation company. From there, indiscriminate selling took over. Many institutions probably couldn’t even own a $100mm market cap company. They had to sell. Their loss, your gain.

I also think there were other factors at play.

Before I explain, I’m going to include another of Greenblatt’s passages:

“Insiders. I may have already mentioned that looking to see what insiders are doing is a good way to find attractive spinoff opportunities. (Okay so maybe I’ve beaten you over the head with it.) The thinking is that if insiders own a large amount of stock or options, their interests and the interests of shareholdings will be closely aligned. But did you know there are times when insiders may benefit when a spinoff trades at a low price? Did you know there are some situations where insiders come out ahead when you don’t buy stock in a new spinoff? Did you know you could gain a large advantage by spotting these situations? Well, it’s all true.

Spinoffs are a unique animal. In the usual case, when a company first sells stock publicly an elaborate negotiation takes place. The underwriter (the investment firm that takes a company public) and the owners of the company engage in a discussion about the price at which the company’s stock should be sold in its initial offering. Although the price is set based on market factors, in most cases there is a good deal of subjectivity involved. The company’s owners want the stock to be sold at a high price so that the most money will be raised. The underwriter will usually prefer a lower price, so that investors who buy stock in the offering can make some money. (That way, the next new issue they underwrite will be easier to sell). In any event, an arms-length negotiation takes place and a price is set. In a spinoff situation no such discussion takes place.

Instead, shares of a spinoff are distributed directly to parent-company shareholders and the spinoff’s price is left to market forces. Often, management’s incentive-stock-option plan is based on this initial trading price. The lower the price of the spinoff, the lower the exercise price of the incentive option. (E.g. if a spinoff initially trades at $5 per share, management receives the right to buy shares at $5; an $8 initial price would require management to pay $8 for their stock). In these situations, it is to management’s benefit to promote interest in the spinoff’s stock after this price is set by the market, not before.

In other words, don’t expect bullish pronouncements or presentations about a new spinoff until a price gas been established for management’s incentive stock options. This price can be set after a day of trading, a week, a month, or more. Sometimes, a management’s silence about the merits of a new spinoff may not be bad news; in some cases, this silence may actually be golden. If you are attracted to a particular spinoff situation, it may pay to check out the SEC filings for information about when the pricing of management’s stock options is to be set. In a situation where management’s option package is substantial, it may be a good idea to establish a portion of your stock position before management becomes incentivized to start promoting the new spinoff’s stock.”

Again, I think this situation played out with Nuvectra. First of all, as detailed above, management’s option package is pretty substantial. It would be in their best interest for the shares of Nuvectra to trade down while their options prices are set.

Greatbatch management and Nuvectra management has been very quiet regarding prospects for the spinoff.

For instance, during Greatbatch’s Q4 2015 earnings conference call, a question was asked about the potential valuation of Nuvectra. Michael Dinkins (Greatbatch CFO), replied, “I think in terms of the valuations, we will let the market determine that. We are quite excited about the products that we are bringing – that they are bringing to the marketplace and that we will be manufacturing for them. But there is a lot of different factors that come into how a startup company will be valued and we will let the market speak on that.” Not exactly a ringing endorsement.

Additionally, Nuvectra didn’t make its investor presentation available on its website until 3/30/2016, exactly two weeks after the spinoff took place. In reaction to the presentation being posted, the stock has rallied +50%. Perhaps, management didn’t want to promote the stock until their options had set. Of course, I could be way off here.

Finally, Piper Jaffray even mentioned that the stock would likely sell off after the spinoff due to indiscriminate selling, a prediction that proved prescient.

“With a sub-$500mm market capitalization, some investors in Greatbatch may view NVTR as too small for their portfolios. In addition, the emerging growth profile of Nuvectra may not match the investment criteria for GB investors given its profile as a large, diversified OEM. Therefore, some GB investors may immediately sell their shares after the spin is effected, creating downward pressure on NVTR shares.”

How much is Nuvectra worth?

Nuvectra Solvency

One of the conditions that needed to be met for Greatbatch to spinoff Nuvectra was the board of directors of Nuvectra had to receive an opinion from an independent valuation firm confirming the solvency acceptable to Greatbatch. While this doesn’t give us a hard valuation number, it is nonetheless, reassuring.

Sale of Minority Interest in Nuvectra

Prior to the fourth quarter of 2015, Greatbatch owned 89% of Algostim and Pelvistim (Nuvectra’s two main products). In the fourth quarter of 2015, Greatbatch purchased the outstanding 11% of Algostim and Pelvistim for $16.7mm. This transaction values those two products at $152mm. Add $68mm of net cash and you have a total value of $214mm. This compares to a current market capitalization of Nuvectra of ~$70mm.

One other point regarding this purchase. Included in that $16.7mm was $6.9mm which was paid to Drees Holding, LLC, which is a limited liability company of the Nuvectra’s CEO Scott Drees. Drees had acquired his interest in Algostim and Pelvistim in connection with a long term consulting contract prior to him becoming CEO in July 2015.

A couple thoughts. I don’t know how Greatbatch got comfortable with the $152mm valuation. Because obviously there are conflicts of interest both perceived and perhaps real. I image Greatbatch’s board of directors got comfortable with the valuation by hiring a third party valuation firm. To cover their liabilities, I imagine they were conservative, but who knows.

Value of Intellectual Property Portfolio

In sum, Greatbatch has spent ~$125mm on Nuvectra which includes past R&D and acquisitions. As a result, Nuvectra has 107 U.S. patents (an additional 77 pending) and 49 foreign patents (an additional 43 pending). Add $68mm of net cash to that prior investment yields a total value of $193mm. This compares to the current market capitalization $70mm.

Piper Jaffray Price Target

Piper Jaffray has a $25 price target on NVTR. Here’s how Piper gets to its target:

“Our $25 price target is based on an enterprise value of 2.7x our FY 2018 revenue estimate of $78.3mm discounted one year at 10%, and assuming $88.7mm net cash and 11.1mm shares outstanding. We feel it is appropriate to value NVTR on 2018E revenue as it encompasses a more accurate portrayal of the enterprise by including revenue from the PelviStim SNS segment as well as allowing for value of a complete, maturing Alogovita SCS salesforce to be reflected.”

For those who are curious, I also ran another valuation analysis looking at Nuvectra vs. its med tech competitors on an Enterprise Value / Sales and Price / Book Value basis. Spoiler alert. It looks cheap.

If you would like to receive this analysis, click on the button below, enter your email address, and I will send it to you.

Click Here for NVTR Price/Book and EV/Sales Analysis

Conclusion

In my view, NVTR is undervalued and represents a very attractive risk reward. It is likely worth significantly more than is currently reflected in its share price. If you have any feedback, comments, pushback, etc, I want to hear it. Please reach out to me on twitter. (@stockspinoffss)

Areas for Additional Work

I want to do some more work on neuromodulation market to gain a deeper understanding of the various players and will post additional details if I find anything noteworthy. If you have any contacts or insights, please let me know.

Disclosure

I currently own NVTR. Please do your own work. This article is not a recommendation is posted for informational purposes only. If you do plan to buy NVTR, please use limits as the stock has very low trading volumes.

Great analysis

what do you think of Q2 results ?

The company will burn 25m$ cash per year, so Algovita have to work (10 market share) in a crowded business (4 competitors)

Thanks for the question. Q2 and Q3 results were good. Algovita revenue continues to grow sequentially. Biggest factor for me is the build out of the sales team. Through Q3, NVTR has hired 42 reps. They are ahead of their plan to get to 50 by year end. Sales rep hiring is a great leading indicator for Algovita sales as sales reps are smart and financially motivated. They would not join a company who’s product they didn’t think they could sell. I p;an to post additional thoughts shortly.

Thanks for the write-up. Really helpful. I just spent some time with C.E.O + C.F.O. who are REALLY impressive guys that I wouldn’t expect at a company this small. They talked candidly about how this came to be and the negotiation with Great Batch leading to the spin, which led me to think the Aleva relationship and Nueronexus could be worth quite a lot (particularly NueroNexus). Considering the money spent developing this and the balance sheet combined with the management and market opportunity, I think this is a strikingly misplaced stock.

I have 2 questions- 1 do you have any thoughts on their agreement with GreatBatch to manufacture the products?. Im concerned its a “sweetheart deal” that might restrict gross margins.

2-Nevro-NVRO (which has 50X the market value and was NVTR’s size a few year ago) has done phenomenally well and claims there HFT technology is vastly superior. I get conflicting reports on this. Do you have any opinion.

Great writeup. Lets see when the market agrees!