Thungela Resources: Buy the Toxic Waste

About a month ago, I recommended that my premium subscribers buy Thungela Resources, a coal spin-off from Algo American.

Since then, I’ve made it my largest personal investment, and it’s currently my highest conviction idea.

The stock is up about 36% since my recommendation, but there is a lot more upside remaining.

Key Statistics

Ticker: TGA SJ / TGA LN

August 20, 2021

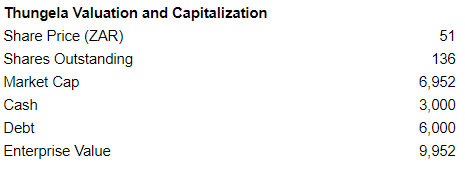

TGA SJ: 51.66 ZAR

Market Cap: 7.0 BN ZAR ($471MM)

Enterprise Value: 4.0BN ZAR

Price Target: 125 ZAR

Upside: 142%

Resources

Thungela Investor Webcast – May 2021

Thungela Investor Day Transcript – May 2021

Thungela Investor Day Slides – May 2021

Twitter Source for Idea: @DeepValueInv

Other Twitter Source for Idea: @AimingHigher4

https://twitter.com/acosgrove003/status/1412249517550977026

Summary

Thungela Resources is a spin-off of Anglo American which began trading in June 2021. The investment case is simple. It’s crazy cheap (1.5x ‘21 current earnings), has no debt, and is going to return significant cash to shareholders.. At current coal prices, I estimate it is generating 916MM SAR of free cash flow per month (14% of market cap). The catalyst is a dividend initiation although we will likely have to wait until year end. Based on guidance from the company (30% payout ratio), I expect the dividend yield to be ~16% at the current stock price although it could be higher. South African peer Exxaro Resources trades at 5.1x 2021 EBITDA. If TGA traded at parity to Exxaro it would be worth 136 (current price is 51). Pick the appropriate discount but TGA is severely undervalued.

Where to Buy Shares

The caveat is this stock doesn’t trade in the United States (I think this is part of the reason why the opportunity exists).

You can buy it through Schwab and Fidelity (I used both brokers).

The security trades in London and Johannesburg (South Africa). Volume is good in both places (~1MM shares traded daily on avg). I bought in South Africa because at the time, trading volume was slightly higher and the fees are slightly lower.

Here are the costs/commissions as I understand them:

Schwab:

- London:

- 0.6% to buy, 0.1% to sell. Plus commission of 0.75% or $100 (whichever is greater).

- Currency charge is embedded in the fee.

- Johannesburg:

- 0.4% to buy, 0.1% to sell . Plus commission of 0.75% or $100 (whichever is greater).

- Currency charge is embedded in the fee.

Fidelity:

- London:

- 0.50% to buy, 0.0% to sell. 1.0% currency conversion charge. Plus GBP commission (unsure what it is).

- Johannesburg:

- 0.25% to buy, 0.0% to sell. 1.0% currency conversion charge. 225 ZAR ($15) commission.

While these fees seem crazy in a world of zero commissions, I’m happy to pay it given the extreme mispricing.

Background

Anglo American PLC (AAL LN) is a $50BN market cap mining company focused on polished and rough diamonds, copper, platinum and other metals.

In April 2021, it announced that it would spin off its thermal coal business into a new company, Thungela Resources, in an effort to transition away from the most polluting fossil fuels.

Thungela Resources began trading on June 7, 2021 in Johannesburg at 21.90 SAR and is up over 100% over the past couple of months.

Nonetheless, the stock is still incredibly cheap and will likely re-rate when a dividend is announced.

Its current market capitalization is ZAR 7.0BN or $471MM.

Business Overview

Thungela is thermal coal business.

Thermal coal or steaming coal is burned for steam to run turbines to generate electricity either to public electricity grids or directly by industry consuming electrical power (such as chemical industries, paper manufacturers, cement industry and brickworks). During power generation the coal is ground to a powder and fired into a boiler to produce steam to drive turbines to produce electricity.

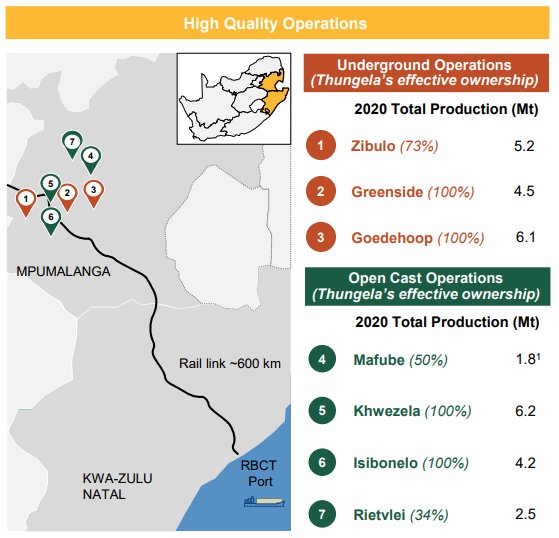

Thungela has 7 coal mines in South Africa as shown below.

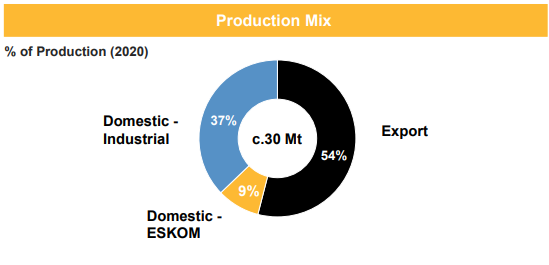

54% of production is exported, 37% is consumed internally in South Africa, and 9% is sold to ESKOM (state owned), the largest producer of electricity in Africa.

Thungela expects demand from Asia to drive growth (Bangladesh, Pakistan, and Sri Lanka).

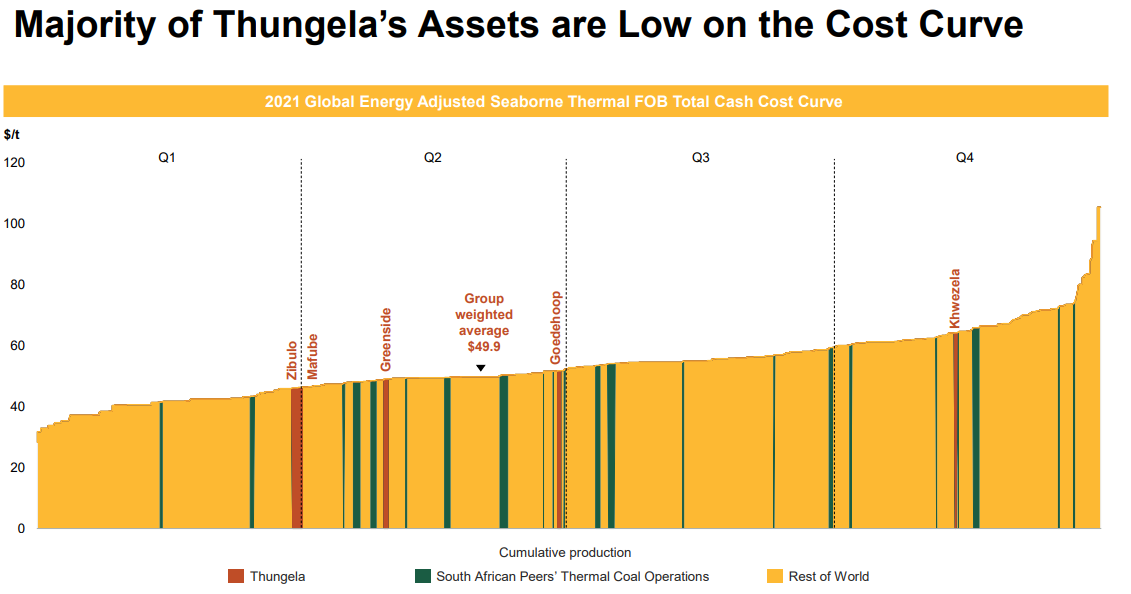

The company believes its mines are on the low end of the global cost curve.

I have no idea if this is true, but if it is, it should provide downside protection if coal prices fall (They are soaring now).

Source: Trading Economics

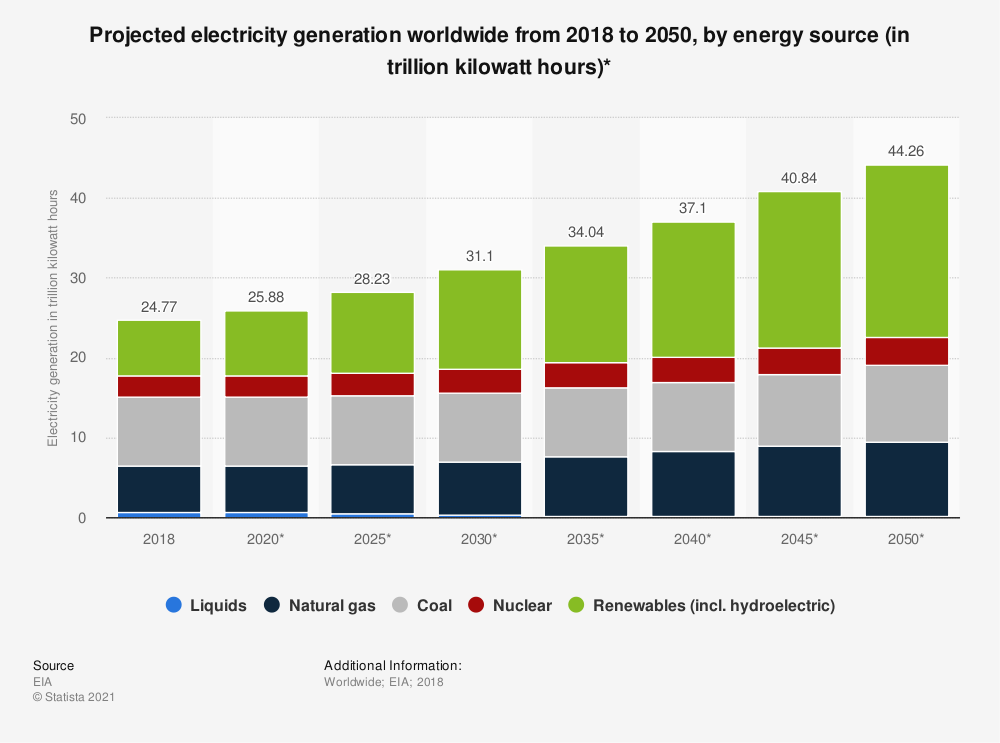

Coal is the dirtiest power generation source but it’s the cheapest. As such, it’s likely to be used for the next 30-50 years. It’s easy for rich regions (U.S. and Europe) to move away from coal for moral / environmental reasons, but developing economies are going to need it to power their economies.

Here is IEA’s forecast for global electricity generation.

Earnings Outlook, Valuation, and Dividend

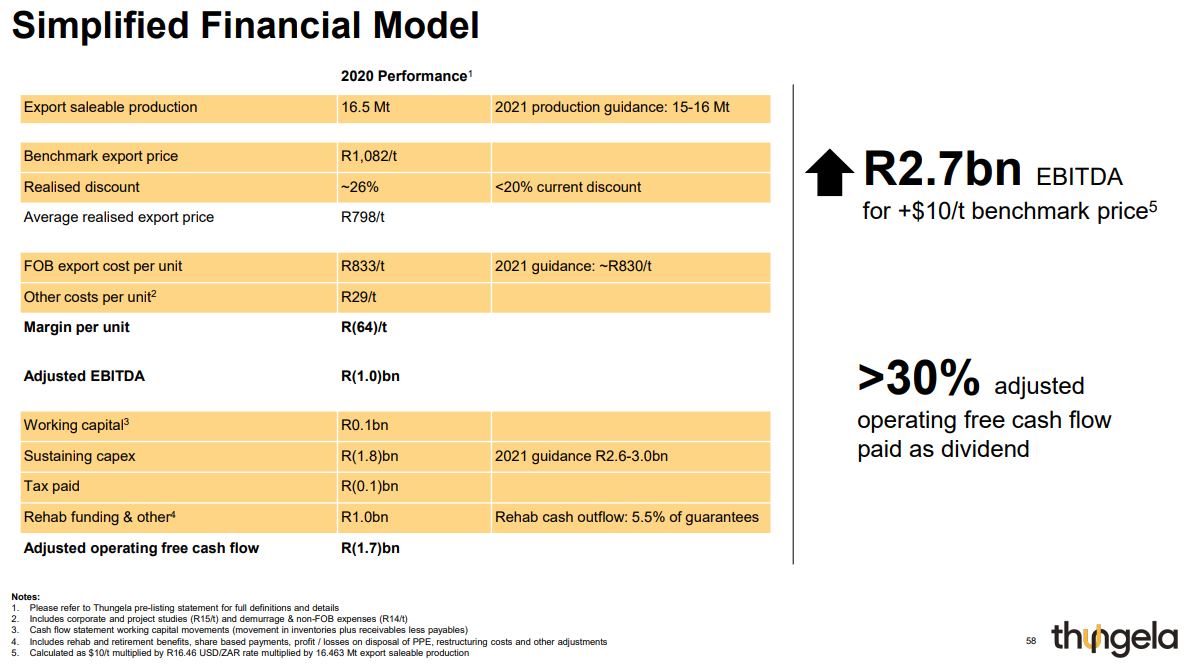

At its analyst day, management noted that every $10 increase in the price per ton of coal will increase EBITDA by R2.7BN (talk about operating leverage!).

In the first half of the year, Thungela earned 1.9BN R of EBITDA.

To be conservative, let’s assume the price of coal is $110/ton on average in the second half of 2021.

This seems reasonable / conservative given the current price of coal. See chart below.

Source: Bar Chart

In this scenario, second half ‘21 EBITDA should be approximately [ 4.5 (($110-$65)/$10) * R2.7BN ] / 2 (½ year) = R6.1BN.

Add this to first half EBITDA of R1.9BN and Thungela is on track to generate R8.0BN.

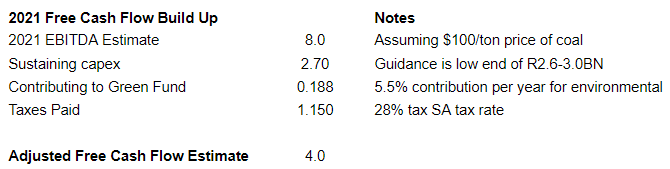

What about free cash flow?

As shown below, I estimate the company will generate R4.2BN of free cash flow.

This free cash flow estimate is probably conservative given coal prices are currently $139/ton vs. my assumption of $110/ton.

Nonetheless, TGA is trading at 1.8x my conservative 2021 FCF estimate.

While that may seem incredibly cheap, it gets even better.

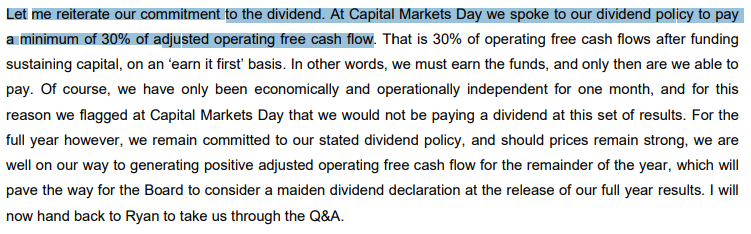

The company has guided that it will pay out >30% of its adjusted operating free cash flow per year as a dividend.

30% of R4.2BN is R1.26BN or a dividend yield of ~25% at Thungela’s current market cap.

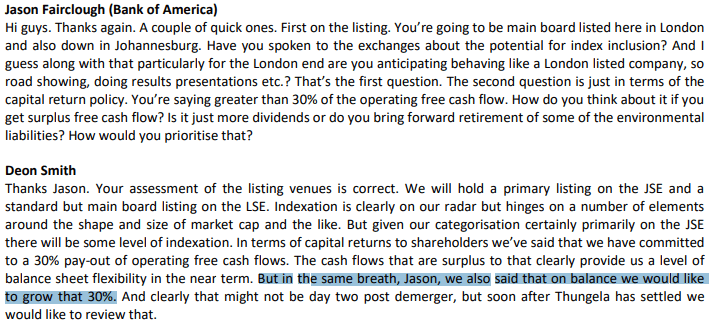

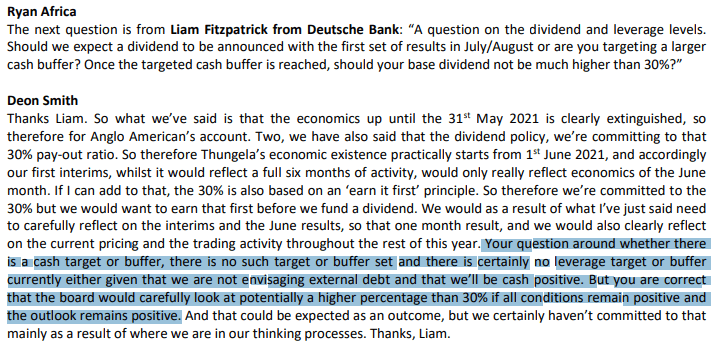

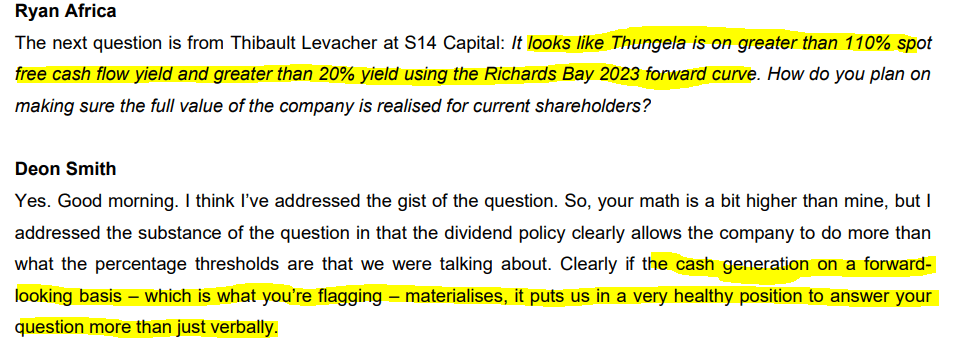

It hasn’t been declared yet but management was very explicit about the dividend during the analyst day. See commentary (including Q&A) below.

When will the dividend be declared?

It’s likely to be declared when Thungela releases its annual results in February (Anglo American, its parent, reported its annual results on February 25, 2021.

Here’s what management said about its dividend on its last earnings call.

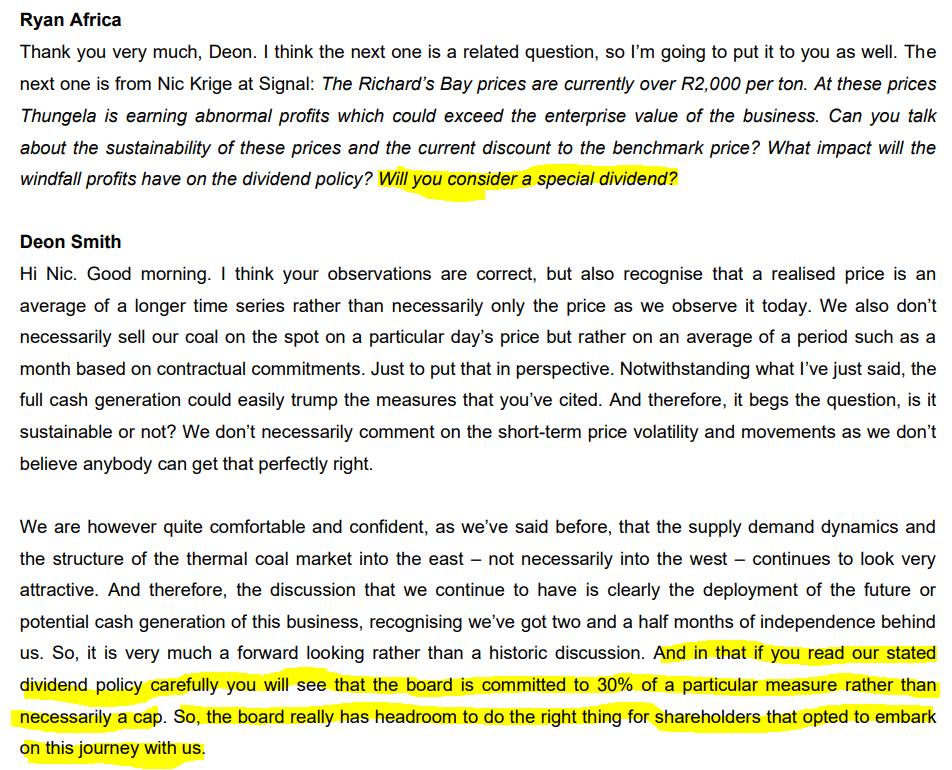

An analyst asked about potential special dividend, and from the answer below, it appears that the board would certainly consider it.

Comps

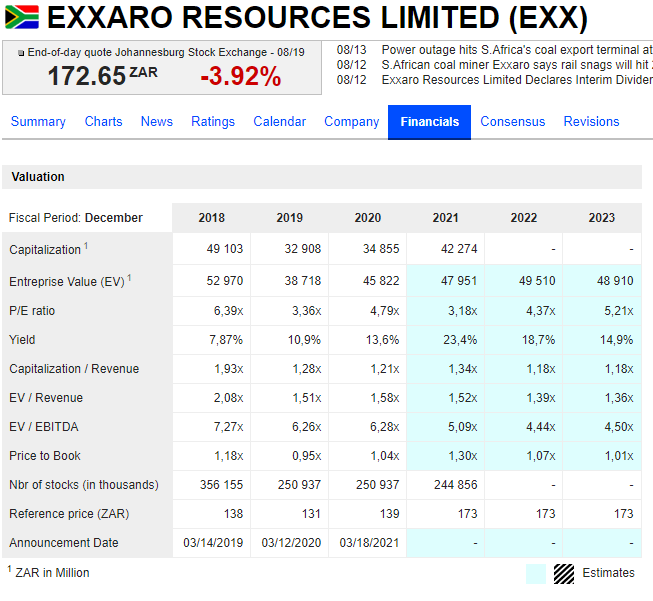

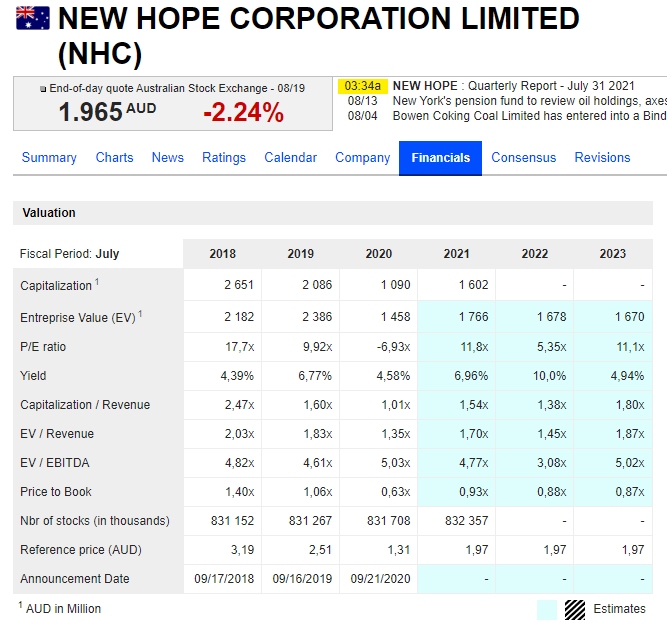

I think the best comps are Exxaro Resources (EXX SJ), another South African coal company, and New Hope Corporation (NHC), a Australian coal company.

Exxaro trades at 5.1x 2021 EBITDA while New Hope trades at 4.8x 2021 EBITDA.

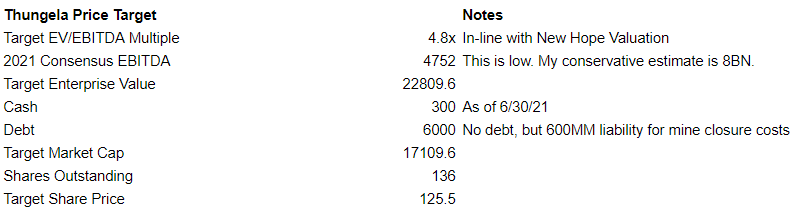

Let’s assume that Thungela deserves to trade inline with New Hope at 4.8x 2021.

In this scenario, Thungela should be valued at 125.50 ZAR per share versus its current price of 51.

Don’t think Thungela should trade in-line with New Hope?

That’s fine.

Pick whatever discount you think is appropriate, and TGA is still undervalued.

Also, note I’m assuming the consensus EBITDA estimates for TGA even though it’s likely off by ~100%.

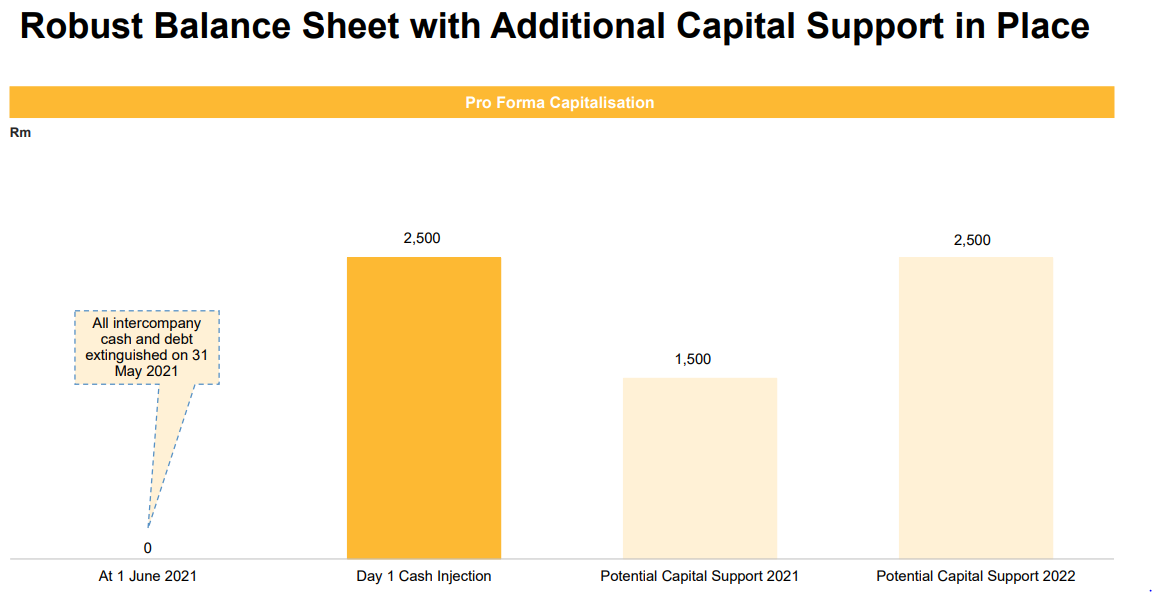

Downside Protection

Thungela has no debt and was capitalized with 2.5BN ZAR (49% of market cap) at the time of the spin-off. In 23z days in June, it added 500MM of additional cash to its balance sheet.

Further, if coal prices retreat, Anglo American will provide additional financial support to the spin-off. I don’t expect this financial support to materialize given how strong coal prices are, but it does provide another measure of downside protection.

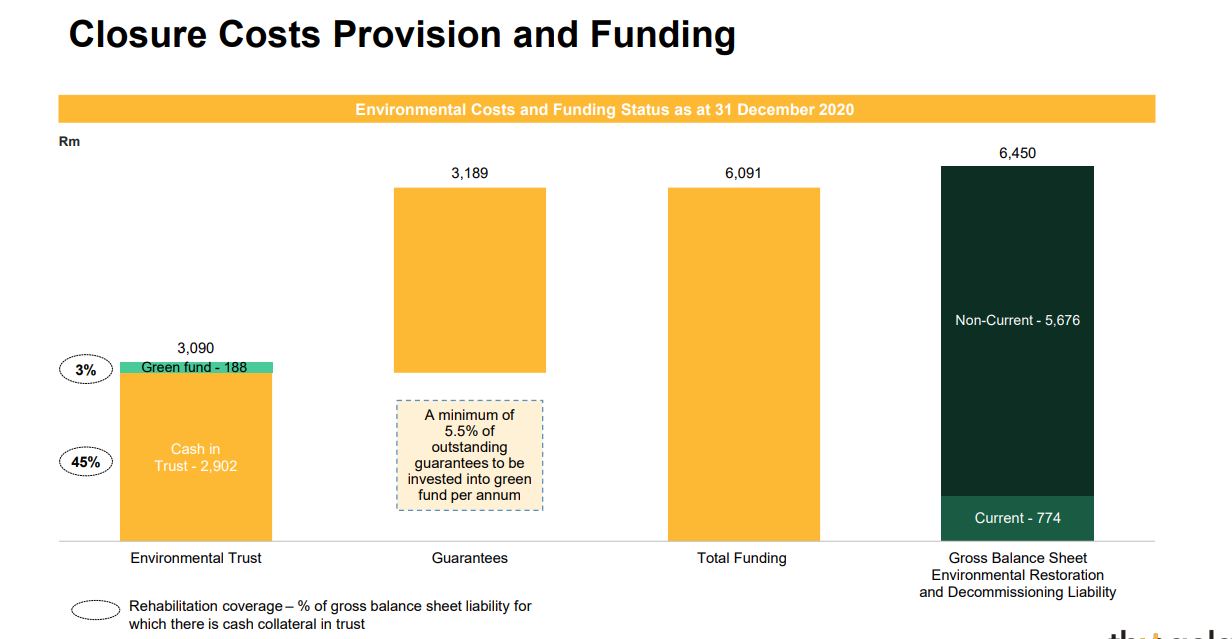

Coal Cost Liabilities

At the time of the spin-off, Boatman Capital Research targeted Thungela with a short report arguing that the company was worthless given its environmental liabilities needed to eventually close down its coal mines.

Boatman Capital closed out its short position profitably, I believe (lucky for them!).

I’m not too concerned about these liabilities at this point.

Thungella has 2.9BN ZAR of cash in a trust to meet its environmental liabilities. It also has an additional 3.2BN ZAR of liabilities which it will meet by contributing 188MM ZAR per year (5.5% of outstanding guarantees) as detailed below.

The environmental issues may become an issue years down the road, but I’m not worried about it in the near term given incredibly free cash flow generation and the large expected dividend.

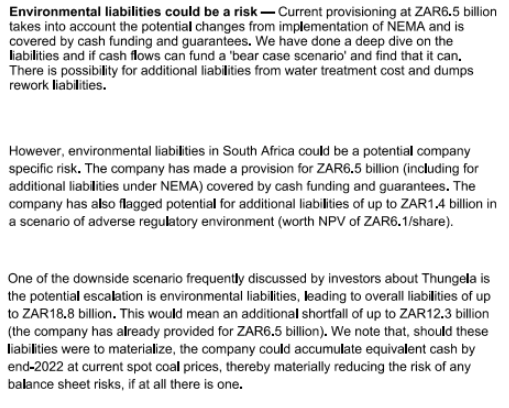

Here’s what Citi has to say about the environmental liabilities.

Conclusion

I think Thungela is an extremely attractive near term opportunity.

Disclaimer/Disclosure

Rich Howe, owner of Stock Spin-off Investing (“SSOI”), owns Thungela shares. All expressions of opinion are subject to change without notice. This article is provided for informational purposes. Please do your own due diligence and consult with an investment adviser before buying or selling any stock mentioned on www.stockspinoffinvesting.com.

THUNGELA – 350% QUICK PROFIT FROM GREEN INSANITY

https://www.undervalued-shares.com/weekly-dispatches/thungela-350-quick-profit-from-green-insanity/aff/9/

Just wondering how much of Thungela is now owned by the South African or other governments and if there is a trend.