Top Ideas for 2021

For the five years prior to quitting in 2018, I worked for a large global investment bank.

I learned a lot and enjoyed the people with whom I worked.

But did I feel like a cog in the corporate industrial complex?

Yep.

The best thing about running your own business is you call the shots.

You can publish whatever you want.

And it attracts like minded people.

People that you wouldn’t be able to meet under any other circumstance.

Tim Ferriss says that his podcast allows him to “punch above his weight.” In other words, he gets to meet and interact with amazing people that he would never otherwise be able to interact with.

I feel the same way about my site.

It gives me an excuse to interact with and exchange ideas with an ever expanding group of talented investors.

In December, I reached out to several of my favorite stock pickers to ask them to share their best idea for 2021.

Some of the stock pickers are anonymous and want to stay that way. Others are well known on Seeking Alpha and Twitter.

My guidance to them was to provide a write up of at least 250 words with their best idea for 2021.

The ideas range from a $552BN conglomerate to a recently issued SPAC to a $14MM market micro-cap (disclosure: I do not own any of these names….yet).

Without further ado, let’s get into their best ideas for 2021.

I will go in alphabetical order.

Enjoy!

Berkshire Hathaway (BRK.A/BRK.B)

Asif Suria, Inside Arbitrage

Twitter: https://twitter.com/AsifSuria

Each week, I eagerly await two separate emails from Asif. The first, Insider Weekend, highlights actionable insider buying and selling. The second, Merger Arbitrage Mondays, highlights recent M&A and attractive arbitrage opportunities. Better yet, it’s free. You can sign up here. Alright, here’s Asif….

We live at an interesting juncture in history right now. It is a time of record disruption from a global pandemic, a time where a vaccine was developed in record time and a time of record stimulus that is fueling multiple bubbles simultaneously. Cautious investors turned bearish well before the bubbles imploded in 2000 and 2007. They gave up some significant gains for a year or two depending on how early they were in calling a bubble but had enough dry powder to invest in companies trading at great bargains after those bubbles burst.

Timing market tops and bottoms is nearly impossible and could cause investors to miss large parts of the market cycle. One of the things active investors can do is look for a divergence between the perceived intrinsic value of an investment and its market price and position yourself to benefit when that divergence closes. It is even better if the company you picked has the potential to do well in the long run and combines the best of both value and growth. In other words, it provides growth at a reasonable price (GARP).

In our quest to find these companies at Inside Arbitrage, we look for various signals and one such signal we have monitored and used actively for over a decade is the buying of stock by company insiders through open market purchases. Considering insiders already derive a large portion of their compensation or wealth from their company’s stock through founder’s shares or option grants, it stands to reason that they would have conviction when they put even more money into the stock through open market purchases. Their conviction also needs to hold true for a period of time because if they sell the stock less than six months from their purchase date, they have to forfeit profits from the trade on account of the “short-swing profit rule”.

If it was this easy to make money following insider purchases, most active investors would do so and the opportunity would be arbitraged away. Unfortunately the signal from insider buying is a little noisy since insiders sometimes buy to “signal the market” and at other times are so narrowly focused on their company that they miss the big picture that the market correctly anticipates. Markets are collectively good at picking up changes in trends, sector specific headwinds and macro cues. To help us hone the signal from insider buying we apply a couple of additional filters to the data including checking if the company is also buying back its own stock and if the company fits our GARP orientation.

Determining the intrinsic value of a company, whether through a DCF model or comparative valuation metrics is challenging because the value you come up with depends on your estimates of inputs that go into the DCF model or the specific valuation metric you use (EV/EBITDA, Price/Book, etc.) for comparative valuation. Most investors would agree that Warren Buffett and his equally wise partner, Charlie Munger, know a thing or two about valuing companies even if they have had a blind spot when it comes to companies that are willing to show losses for years in the quest to capture entire markets. This might explain why Berkshire Hathaway changed the rules on when they buy back their own stock. In their 2019 annual report, the company mentions:

“For several years, Berkshire had a common stock repurchase program, which permitted Berkshire to repurchase its Class A and Class B shares at prices no higher than a 20% premium over the book value of the shares. In 2018, Berkshire’s Board of Directors authorized an amendment to the program, permitting Berkshire to repurchase shares any time that Warren Buffett, Berkshire’s Chairman of the Board and Chief Executive Officer, and Charlie Munger, Vice Chairman of the Board, believe that the repurchase price is below Berkshire’s intrinsic value, conservatively determined. The program continues to allow share repurchases in the open market or through privately negotiated transactions and does not specify a maximum number of shares to be repurchased.”

If Mr. Buffett and Mr. Munger know how to determine the intrinsic value of most companies, they quite clearly must know how to determine the intrinsic value of their own company. But just in case they make a mistake, they decided to add a margin of safety as indicated by the words “conservatively determined”. They used this flexibility to buy, not just when the stock was trading below 1.2 times book value but when they perceived it was a good buying opportunity, to good use in 2020. As we mentioned in our last insider weekends article, according to Bloomberg,

“Berkshire Hathaway Inc. spent the third quarter buying back about $9 billion of its own stock, more than it had repurchased in any full year in its history. The buying spree takes the total repurchases in the first nine months of 2020 to $16 billion”

What really caught my attention was an unusual insider purchase at Berkshire Hathaway by one of its long-serving directors. Director Ronald L. Olson spent nearly $900,000 to acquire 4,000 class B Berkshire Hathaway shares at $222.33 per share. He filed this purchase with the SEC last week but the purchase occurred in December.

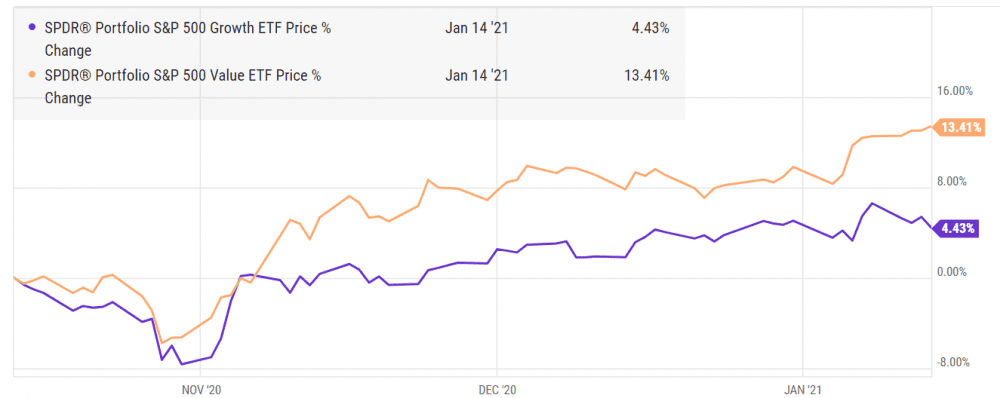

This purchase provided the double signal I often look for where the company is buying back shares while the insiders are independently buying on the open market as well. The icing on the top is that it is Mr. Buffett and Mr. Munger signaling to us that the stock is trading at a discount to its intrinsic value. I also like the stock as it aligns well with the shift from growth to value that we have seen over the last three months as you can see from the chart comparing the S&P 500 Growth ETF (SPYG) with the S&P 500 Value ETF (SPYV).

We have been repositioning ourselves for several months by taking some profits from our high performing technology stocks like Twilio (TWLO) and buying companies like B. Riley Financial (RILY) and Mohawk (MHK) that were trading at attractive valuations. If and when this bubble bursts or decides to flatline, a company like Berkshire Hathaway may provide shelter from the storm and you end up getting exposure to a large number of private businesses that have not been bid up to crazy heights in the public market. If exposure to a high growth and high margin technology business is important, you also get a piece of that through Berkshire’s stake in Apple, which was worth $111.7 billion as of September 30, 2020. We decided to pick Berkshire Hathaway as our pick for 2021 because it is attractively valued and provided us multiple positive signals through insider buying and the company buying back its own stock.

Asif Suria

Founder and Editor

Inside Arbitrage

https://www.insidearbitrage.com

Disclosure: I do not hold a position in Berkshire Hathaway but plan to initiate a position after this article is published. Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.

Information Analysis Inc (IAIC)

Maj Souedian, GeoInvesting

Twitter: https://twitter.com/majgeoinvesting

Maj is an absolute legend in the micro-cap world. He is a full time investor and has generated amazing returns over his life. He runs a service called GeoInvesting which you can trial for free. I’m a happy subscriber :) Here’s Maj….

$25 Million Contract Resurrects Information Analysis from The Dead

Information Analysis Inc (OTC:IAIC) is a provider of information technology services to the private sector as well as government clients. The company generates its revenue from selling third party software and fees from programming/project services performed by its employees.

IAIC is the classic case of a high quality microcap company just hanging around for a growth catalyst to arrive. I see mutli-bagger potential in shares of IAIC.

Brief History

Founded in 1979, IAIC uses software and its full-time programmers to modernize legacy/outdated IT systems. Most of the company’s revenues are generated from the U.S. federal government and state and local governments, but commercial markets are also being pursued.

IAIC has performed IT modernization and electronic forms conversion projects for over 100 commercial and government customers. IAIC has been struggling to grow revenue and net income for years. The company’s revenue has generally been in the range of around $5 to $10 million since 1995, while EPS has been dancing around break-even since 2008.

For years, IAIC’s growth had suffered from a lack of urgency by government agencies to improve and replace outdated IT systems, despite the fact that in recent fiscal years, the federal IT budget has been over $90 billion annually. However, according to Government Accountability Office’s (GAO) 2019 budget document, over 80% of all IT spending is on the Operations and Maintenance:

“aging legacy systems, which pose efficiency, cybersecurity, and mission risk issues, such as ever-rising costs to maintain them and an inability to meet current or expected mission requirements”

Well, government agencies can’t sit around doing nothing forever. For example,10 critical legacy government agency IT systems range in age from 8 to 51 years old, including those dealing with national security. But I believe that a high probability exists that government agencies have reached a tipping point where they will have to upgrade outdated IT infrastructure, especially when considering that that the coronavirus pandemic has exposed weaknesses in government agencies’ technology infrastructures like:

- Health care bottlenecks

- Procurement and distribution issues for personal protective equipment

- Processing unemployment claims

- Processing stimulus checks

- Processing SBA and disaster loan applications.

I believe that a key driver of growth and profitability for IAIC will be the increasing focus on the modernization of legacy IT systems by U.S. government agencies.

Tides Are Turning

IAIC reported Q2 2020 revenue of $4.8M, up 30% YOY, its highest quarterly revenue performance since 1998.For Q3, revenues rose 25% to $3.9 million and EPS came in at 2 cents compared to a loss.

These results are primarily due to the company beginning to service a large federal government agency contract which had been delayed due to a protest from the incumbent who eventually lost the contract to IAIC

In April 2020, the incumbent withdrew the protest, paving way for IAIC to commence work on the contract.

The coronavirus pandemic had also impacted the commencement of services under the new contract for a few months, with IAIC finally starting project work on June 1, 2020. The new contract is part of a government modernization program to be carried out over a 7-year term and is potentially worth $25 million, which will enable the company to generate a healthy base of consistent profitable revenue for several years, serving as a basis from which it can invest in growth opportunities.

“We anticipate that these contracts will provide a solid foundation of revenue and profitability for the foreseeable future.” CEO

Also, old government databases are programmed in COBAL and it is getting increasingly difficult to find COBOL programmers, which plays right into IAIC’s advantage of being “fully stocked” with COBOL programmers.

Potential Margin Expansion

Gross Margins

The company has two main sources of revenue – third party software license revenue, and professional fee revenue. Software sales have 3 components:

- Sales of third-party software licenses and implementation and training services

- Sales of third-party support and maintenance contracts based on those software products

- Incentive payments received from third-party software suppliers for facilitating sales directly between that supplier and a customer introduced by the Company

Professional services consist of “developing and maintaining IT systems for government and commercial organizations” (programming, database structure and project management).

Typically, professional fees have accounted for the majority of revenue until 2016, after which they started to decline.

The gross margins on the software revenue have been quite volatile and are currently near historical lows, sitting under 3% since 2017. Compared to this, the professional fee gross margins are much higher and more stable, ranging from 20% to 45% range. It’s nice to see that professional fee margins have been holding at around 40% since 2009.

The new $25 million contract revenue will mainly consist of high margin professional fees. As such, we anticipate a meaningful profitability bump for some time, which new contracts will add to, since new contracts carry higher margins than older contracts.

Overall Operating Margins

Aside from a potentially better gross margin profile as a result of the new contract win, Q2 highlighted that IAIC experienced a tremendous amount of operating leverage with operating expenses decreasing 25%, even as sales rose 30%. Likewise, in Q3, operating expenses fell 27% on a 25% increase in sales.

Reduce Dependency on Third Party Software

If the company takes steps to develop and sell its own software solution, software gross margins could increase from the less than 3% range to well over 50%. I do not know if the company is going this route since Oracle plays a big part in their project work, but I did bring it up in a conversation I had with management.

Reduce Dependency On Subcontracted Work

A good deal of IAIC’s contract wins comes through subcontracted work. Going after contracts directly would allow IAIC to capture more margin.

Penetrate Commercial Markets

The company generates the majority of its revenues from government agencies. As of Q2 2020, US government agencies generated 79.3% of IAIC’s revenue, subcontracts under federal procurements generated 19.9% of revenue, and commercial contracts generated 0.8% of revenue. I need to gain a better understanding of the commercial market opportunity, but I presume it would come with more favorable and predictable margins.

I also need to learn more on the growth potential of the company’s staffing and electronic forms business and what that could mean for margins. I am also intrigued that the company mentions robotics process automation in its SEC filings as a potential market.

Valuation

IAIC was recently trading at 0.6x sales, but has expanded to around 1x sales on the heels of the new contract win. While this may not seem cheap for a company with a heavy emphasis on government contracts, I think sales will rise by multiples in the future as the company is in the best position it has ever been to aggressively focus on going after new government and commercial contracts, as well as exploring acquisition opportunities. Eventually, investors should be able to value the IAIC on earnings. However, that time may come sooner than you think. Since the new contract appears to be a professional fee contract, we might be able to assume that associated gross margins will be at least 40%. That revenue alone could equate to annual EPS of $0.10. I see multibagger returns over time.

Caveats

- The stock has risen sharply over the past few weeks.

- A prolonged economic downturn due to COVID-19 or a more aggressive second (or third or fourth!) wave of infections could delay contracts, thereby impacting sales.

- Growth prospects are tied to government funding for modernization of legacy IT systems. Any reduction in that could adversely impact the business.

- There is no guarantee that IAIC will earn the top end value of the new contract award.

- The rising competitive intensity remains a risk. IAIC competes with many large players who are more established and have greater financial resources.

- The stock is extremely illiquid.

NexPoint Strategic Opportunities (NHF)

Twitter: ClarkinM

Clark Street Value is one of my favorite investing resources on the planet. And incredibly, it’s free. The anonymous author goes by “MDC” and has a full time job, a family, but has somehow had the time to publish his investment ideas since 2011. Since 2011, he’s generated an internal rate of return (similar to average annual return) of 24.3%!! Don’t tell MDC, but I would happily pay for access to his blog. Here’s MDC…

NexPoint Strategic Opportunities (NHF) is currently a closed end fund (“CEF”) that recently announced it will convert to a diversified real estate investment trust (“REIT”) in 2021. NHF trades at $11.00 versus its stated net asset value (“NAV”) of $18.72 per share, or said another way, NHF trades at just 58% of NAV. To fully understand the opportunity, it is worth looking back at NHF’s 2015 spin-off of NexPoint Residential Trust (“NXRT), NHF had incubated the NXRT strategy inside of NHF before spinning it off as a separately traded REIT.

NXRT is a multi-family REIT that implements a value-add strategy, they buy Class B suburban apartments and add small renovations like new countertops or bathroom upgrades to drive rent growth. Once the low hanging fruit capex has been implemented, they’ll sell the property and recycle the proceeds back into additional value-add properties. NXRT has 5x’d since it started trading separately.

Similarly, NHF has been incubating another private REIT inside of NHF, NexPoint Real Estate Opportunities (“NREO”), instead of spinning NREO out, the management team decided to convert all of NHF into a REIT. NREO’s assets could give a clue to what NHF will ultimately look like, NREO has investments in hot real estate sectors like single family rentals, self-storage, and then more COVID-affected assets like a new-build Marriott hotel and office building, both in Dallas where the management team is based.

By following a similar value-add strategy as NXRT, NHF will be selling non-real estate assets near NAV, investing those proceeds into a post-covid distressed real estate world, improving them, and recycling that capital back into additional opportunities. That creates a multiplier effect which could be quite powerful and drive outsized returns.

For a deeper dive, you can check out my full write up.

PVA TePla (TPE.DE)

Twitter: HRouge

HRouge is one of my favorite follows on Twitter. Do yourself a favor and follow him ASAP. His portfolio has compounded at ~28% over the past 9 years. Here is an example of why you need to follow him. On March 24, 2020, he tweeted out that Etsy looked like an “obvious long term should’ve-been-obvious-in-hindsight winner.” Etsy is up 434% since then 🤣. Here’s HRouge…

At 3x EV/sales and little known beyond Germany, €420M cap PVA TePla (TPE.DE) deserves a closer look.

It contains a unique asset potentially worth much more than the current cap but which is masked by a low-multiple division. In the near-term the company benefits both from an industrial upturn and the coming upcycle in semiconductor capex spending.

It’s all easily missed from the headline figures: 9 months ‘20 actual and guided FY20 revenues of €96M and €130M are both flat YoY, with a small rise of €1M in EBITDA to €17M. Pre-Covid, the two years through to 2019 saw a 53% rise in revenues from 2017 with EBITDA tripling.

One-third of revenues and 21% of pre-corp (excluding corporate costs) margins are industrial systems which have performed admirably through Corona (-2.8% 9M YoY), but for simplicity, I assume a value of 1x 2019 €45M revenues here.

The majority (two-thirds) of PVA is in systems for semiconductor wafer production and metrology, which tests and inspects wafers during and after production – increasingly important as new process nodes have high and expensive wastage rates.

The unique asset is their specialty in the indispensable material for EVs: Silicon Carbide (SiC)

[see an example here]. SiC isn’t blue-sky dreaming, it’s becoming reality. Indeed, Tesla’s demand alone for SiC content is already such that they have invested in production capacity as third-party supply struggles to meet even their demand.

PVA is the only independent supplier of SiC crystal growing systems in the world.

Ex-industrial, ex-cash you can buy that asset for 4x 2020 sales at a 15% EBIT margin. Given the price and potential here for growth, operating leverage and multiple expansion, PVA is my pick for 2021.

Spinning Eagle Acquisition Corp (SPNGU)

Chris DeMuth, Jr., Sifting the World

Twitter: ChrisDeMuthJr

Chris is one of my favorite investors in the world. He has over 30,000 followers on Seeking Alpha and his Sifting the World service is one of the most popular on the site. Chris is prolific. He is somehow able to identify attractive special situations on almost a daily basis. This is my favorite article of his. It talks about how you can find special situations with no risk in everyday life. Here’s Chris…

My 2021 top spin-off pick is Spinning Eagle Acquisition Corp. (SPNGU). I’m participating in the IPO and it will trade publicly within the next few days. Initial shareholders pay $10 per unit. Units include a free call and a free put.

Free call: We get a fifth of a warrant (SPNGW) with a five year term and an $11.50 strike price.

Free put: More importantly, at least to me, is the downside protection. They are raising $1.5 billion from me and others and putting that $1.5 billion in a trust.

We can choose to redeem at that trust value if we don’t like the deal that they pick. So if everything goes horribly wrong, we get $10 (and change, but not much change given the low interest rate environment and the money sits in short-term T bills). Given that unit holders are long put and call equivalent, we are long volatility. I like that bet. Looking at the sponsor’s last four deals, all of which launched units at $10, two equities doubled, one is a five-bagger, and the fourth is trading beneath $2. Three wins and a loss for anyone that didn’t redeem; three wins and a tie for anyone that did.

Many fellow value investors sniff at the aesthetics of SPACs (we’re just not used to liking anything temporarily in fashion) without focusing on the fact that we get a “do over” with our capital if we don’t like the deal target. Were that the case with all my investments. This one even has a spin-off angle! Whatever cash that they don’t need for their deal gets spun-off into a new baby SPAC. So we could get multiple deal premiums… or our money back.

Chris DeMuth, Jr.

So there you have it.

A top idea from 5 of my favorite investors.

To summarize:

Berkshire Hathaway (BRK.A/BRK.B)

Asif Suria, Inside Arbitrage

Twitter: AsifSuria

Information Analysis Inc (IAIC)

Maj Souedian, GeoInvesting

Twitter: MajGeoinvesting

NexPoint Strategic Opportunities (NHF)

Twitter: ClarkinM

PVA TePla (TPE.DE)

Twitter: Hareng_Rouge

Spinning Eagle Acquisition Corp (SPNGU)

Chris DeMuth, Jr., Sifting the World

Twitter: ChrisDeMuthJr

Leave A Comment