I was first attracted to AFI because it’s a small cap spinoff, and small cap spinoffs tend to outperform the market and outperform other spinoffs, as I’ve noted in prior write-ups. https://stockspinoffinvesting.com/stock-spinoff-performance-by-market-cap/

After reviewing AFI’s form 10, AFI’s analyst presentation, and the flooring sector, I’ve concluded that AFI has limited downside and the potential to return +138% over the next four years.

Background

Armstrong Flooring (AFI) was spun out of Armstrong Worldwide and was considered the bad business. Armstrong’s ceiling business was considered the good business.

Why is the flooring business considered the bad business?

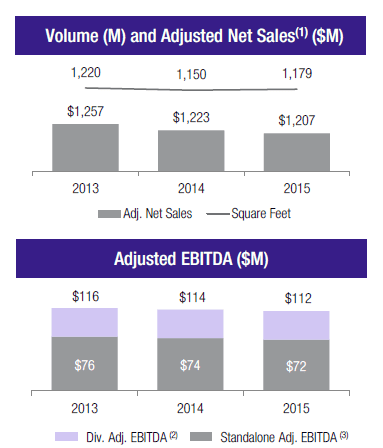

As you can see from the chart below, flooring revenue and EBITDA has trended flat to down over the past three years.

In addition, the margins in the flooring business are a lot lower than the margins in the ceiling business. For instance, in 2015, the flooring business had an EBITDA margin of 6.0% while the ceiling business had a 23.5% EBITDA margin.

So why am I interesting in the flooring business?

AFI’s business is benefitting from new management and its turnaround is well under way.

For instance, in each of the past two quarters (Q4 2015 and Q1 2016), EBITDA has grown double digits. This is very significant as EBITDA declined 2% in 2015. In addition, in Q1 2016, revenue grew 9.6%.

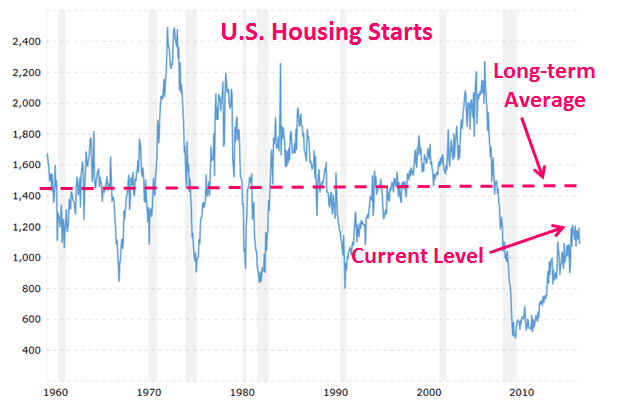

Additionally, the flooring market is benefitting from a healthy housing market.

While the US housing market has increased significantly off its lows, it is nowhere close to prior peak levels. From 1959 to 2016, housing starts (number of new residential construction projects) in the US averaged 1,442. As seen in the chart below, the current level of housing starts remains below the long term average.

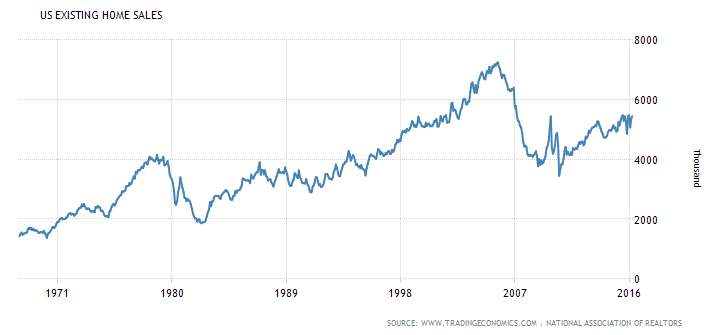

50% of AFI’s sales are driven by renovation of existing homes. These sales strongly correlate to US existing home sales. As such, the chart below, which shows that US existing home sales are well below prior peak, is encouraging.

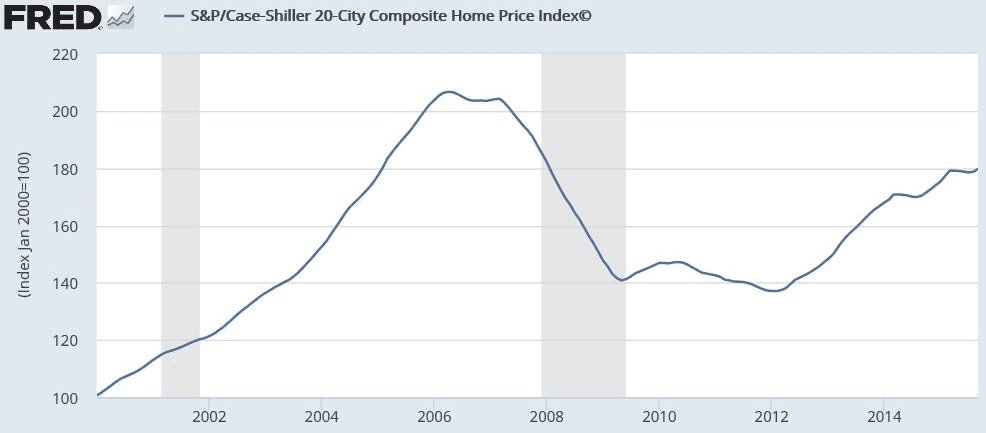

Additionally, the S&P/ Case Shiller Index shows home prices remain significantly lower than the previous peak.

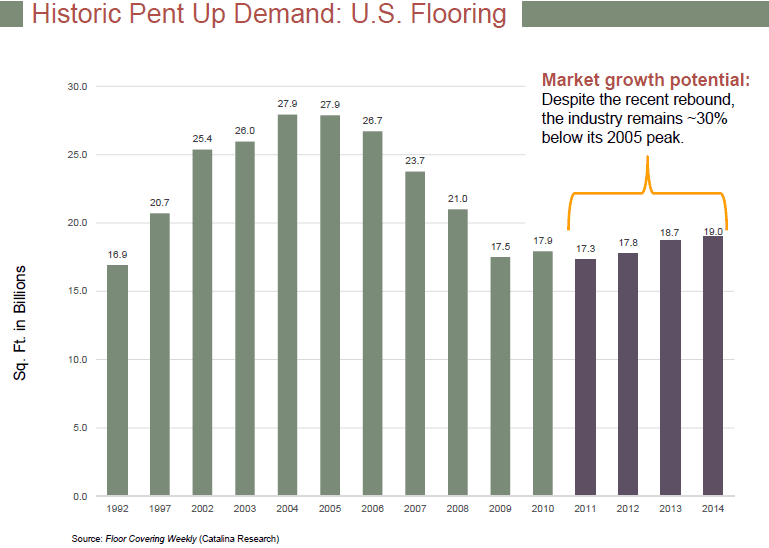

Finally, the U.S. flooring market remains ~30% below prior peak (chart from Mohawk Industries):

Overview of Armstrong Flooring

As described early, Armstrong Flooring sells flooring products for use in construction and renovation of residential and commercial buildings. 92% of sales is generated in the U.S. while 8% is generated in Asia Pacific. As seen in the chart below, 65% of sales is from the residential market while 25% is from the commercial market. In addition, 75% of sales is for renovation while 25% is for new construction.

AFI has two different segments, Resilient Flooring and Wood Flooring.

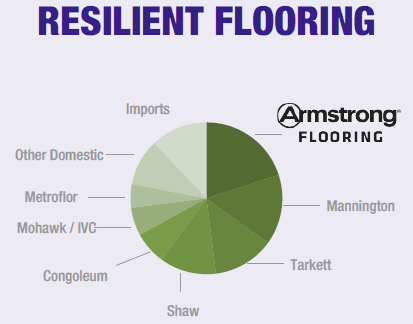

Resilient Flooring (60% of total sales, 65% of EBITDA)

This segment manufactures and sells a broad range of floor coverings. Products include: vinyl sheet, vinyl tile, and luxury vinyl tile.

See picture below for example of Armstrong Resilient Flooring products:

Armstrong is a market leader in the resilient flooring market:

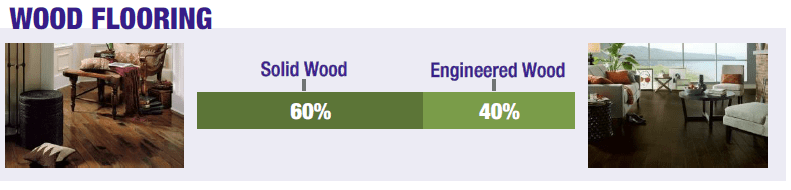

Wood Flooring (40% of total sales, 35% of EBITDA)

This segment manufactures and sells a broad range of flooring products. Products include pre-finished solid and engineered wood floors in various wood species. Virtually all sales are in North America

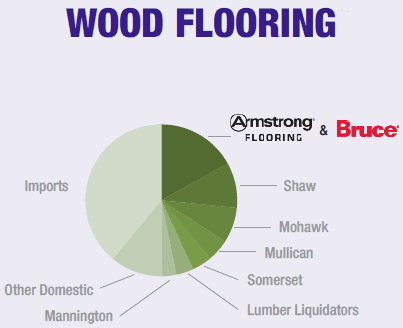

See pictures below of Armstrong Wood Flooring products:

As shown below, Armstrong is a leader in the flooring business.

Prospects for Revenue Growth

Management’s medium term guidance for revenue growth is 5% to 6% annual growth. This is a significant increase from the last three years. Over the past three years revenue has declined ~2% per year. How is AFI going to achieve such a turn around?

First of all, the CEO of AFI, Don Meier, has extensive experience turning around companies at TPG (major private equity company), Freescale Semiconductors, and Hillenbrand Industries. As such, he seems well suited for the job.

AFI has spent that last couple of years reaching out to its distributors (AFI’s customers) to talk about the Armstrong brand and how Armstrong could better serve its customers. AFI has about 1/3 share of wallet among its distributors and it believes there is significant opportunity to better serve those distributors by supplying a broader array of products. By doing so, AFI could capture a larger share of wallet.

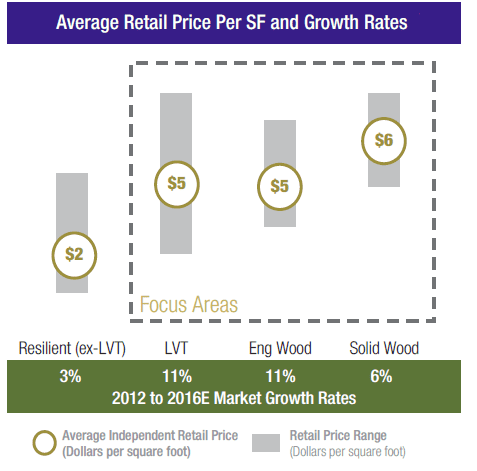

Additionally, AFI has invested in new product innovation and has focused on higher growth markets such as Luxury Vinyl Tile and Engineered Wood whose markets are both growing at 11%. Recently, AFI is benefitting from that investment as its Luxury Vinyl Tile and Engineered Wood revenue is growing faster than the market. In Q4 2015 and Q1 2016, AFI’s engineered wood sales volume increased by 20% and 32%, respectively. During the same quarters, AFI’s Luxury Vinyl Tile sales volume increased by 34% and 42%, respectively. This is having a transformative impact on AFI. In Q1 2015, revenue grew by 10%, a meaningful increase from the 2% revenue decline in 2015.

Additionally, AFI is winning industry awards for its flooring products. Recently, AFI won “Dealers’ Choice Awards” for four separate categories: laminate, hardwood, Luxury Vinyl Tile, and resilient sheet. It is only the second time in the past twenty years that one manufacturer has won in four separate categories. Importantly, the winners were determined by the dealers (Armstrong’s customers). Clearly, AFI’s efforts are paying off.

Opportunity for Increased Margins

As mentioned earlier, AFI currently generates an EBITDA margin of 6%. Over the medium term, management believes the margin can increase to 10%, which would be more in-line with peers.

How will margins increase so meaningfully?

First of all, AFI’s highest growing products are its highest margin products. As such, AFI is benefitting from a positive mix shift. The chart below displays this trend nicely.

Second, AFI expects to benefit from increased scale as revenue growth accelerates.

Third, AFI has instituted a culture of continuous innovation.

Here are a few examples of how this culture can save costs and improve margins.

Example 1: AFI had just launched a new oversized tile product. However, the tile was too big to be packed on the manufacturing line and had to be packed manually. The AFI team re-engineered the production process so that the product could be packaged on the existing manufacturing line. This reduced labor costs and increased efficiency. AFI estimates this change will save $500,000 per year.

Example 2: Management brought together a group of cross functional individuals to brainstorm how to improve the solid wood manufacturing processes at the company. The individuals were able to improve manufacturing processes such that the company was able to decrease the number of daily shifts from three to two. AFI expects this to generate $5mm of savings per year.

Valuation

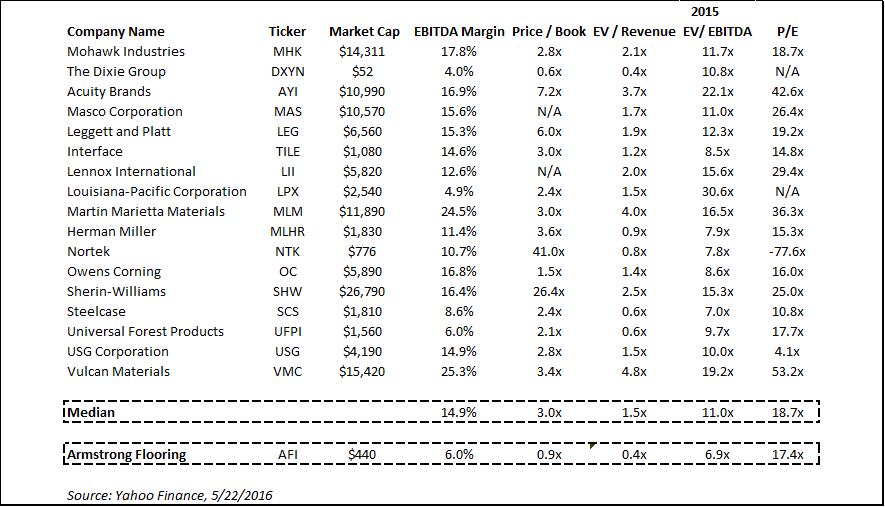

Below, I’ve included a comp table for AFI.

As you can see, AFI looks cheap on all metrics. Direct comps are hard to find in the flooring industry because so many companies are private or have been acquired (more on that below). Now, the above comp sheet is a bit aspirational in many of the companies included have significantly higher EBITDA margins than AFI. However, it does show that AFI should experience valuation expansion if it can improve its margins.

Management’s medium term goals (3-5 years) is to grow revenue 5% to 6% and to achieve 10% EBITDA margins. Let’s assume AFI is successful over the next four years and achieves management’s targets. Revenue would have grown by 5% per year for four years to $1,467mm. EBITDA, benefiting from margin expansion will have grown to $147mm. Applying a 9.0x EV/EBITDA (still at a discount to peers), would yield a $1,320mm enterprise value and a market cap of $1,260mm. I further assume shares outstanding increase by 20% over the period which implies a share price of $37.92, approximately 138% above the current share price.

Precedent Transactions

I recently read a Barron’s article that highlighted shares of Mohawk Industries (ticker: MHK). Mohawk is an industry leader in the flooring market.

One section in the article caught my eye: “Mohawk Industries, the top U.S. flooring company, is benefitting from a healthy housing sector and a knack for scooping up smaller players and increasing their profit margins…..speaking of acquisitions, Mohawk has spent $3.5 billion on them since 2013….on the latest earnings call management indicated that Mohawk’s balance sheet could support an additional $1 billion to $1.5 billion in debt.”

It’s not a difficult stretch to connect the dots back to AFI. It would be a lovely acquisition for Mohawk. AFI’s EBITDA margins are 6.0% while Mohawk’s are 17.8%. If AFI’s turnaround strategy doesn’t work, I’m sure Mohawk would love to swoop in to acquire AFI.

One other interesting point. In AFI’s Form 10, the company highlights the following risk: “Potential for takeover: As a smaller company, AFI may be at increased risk to become the target of a takeover on terms that are not in the best interests of AFI or its shareholders.”

This seems like an odd risk to highlight. From my point of view, the potential for AFI to be acquired is a major positive and providers a measure of downside protection.

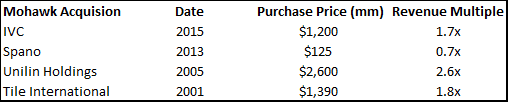

What prices has Mohawk historically paid?

Here are the acquisitions that I could find:

AFI currently has revenue of $1,200 and trades at an EV/EBITDA of 0.4x. While the above list isn’t exhaustive it does suggest that AFI’s acquisition price would be at a significant premium to current valuation.

Downside

From my perspective, the risk would be that the turnaround fails. However, if that were the case, I think it’s highly likely that the stock would be acquired by Mohawk or another larger competitor.

The other big risk is that the housing market is about to roll over. The data that I’ve viewed doesn’t suggest that is the case, but who knows.

The good thing is AFI trades at a cheap valuation and has very little debt. As such, the downside should be limited even if the turnaround fails or if the housing market turns down. As such, I believe the risk/reward is very favorable.

Other Points

- The CFO of Armstrong Holdings chose to go with the smaller spinoff as COO. It’s usually a good sign when management leaves the parent company to go with the spinoff as it implies he/she thinks it is an attractive opportunity.

- ValueAct (well-regarded hedge fund) owns 16% of the company and has a board seat. We can ride their coat tails.

- Raging Capital (hedge fund with 20% annual returns) just announced it owns 6% of AFI. Another vote of confidence in the opportunity.

- AFI’s Form 10 discloses that 19% of shares outstanding are reserved for executive compensation. I view this as a huge positive as management is heavily incentivized to increase the share price.

- Remember what Joel Greenblatt wrote: ““Insider participation is one of the key areas to look for when picking and choosing between spinoffs – for me, the most important area. Are the managers of the new spinoff incentivized along the same lines as shareholders? Will they receive a large part of their potential compensation in stock, restricted stock, or options?”

Additional info:

Link to Form 10: http://ir.armstrongflooring.com/Cache/33346858.pdf

Link to Management Presentation: http://ir.armstrongflooring.com/Cache/1001208656.PDF?O=PDF&T=&Y=&D=&FID=1001208656&iid=4660935

Link to Q1 2016 webcast: https://viavid.webcasts.com/viewer/event.jsp?ei=1100402

Great and.compelling.write up. Keep it up

Many thanks Nick!

I quite like looking through an article that will

make people think. Also, thanks for allowing me

to comment!