After doing some work on QHC, I bought the stock based on the thesis that I outline below. Unfortunately, last week QHC reported a VERY DISAPPOINTING quarter the stock dropped by roughly 50%. I’ve sold out of the stock and cut my losses. The purpose of this post is to review my thesis and evaluate lessons learned.

Background

Community Health Systems (CHS) began as a non-urban company of small and rural hospitals. Over time, CHS acquired Triad and HMA and grew to be 194 hospitals in 28 states. Over time, the primary focus changed to focusing on larger, urban hospitals, regional networks, and leveraging centralized systems across the hospital network.

In May 2016, Community Health Systems (CHS) spun off Quorum Health Services (QHC). The spinoff was designed split the company into two different hospital stocks. CHS would focus on urban hospitals while QHC would focus on more rural hospitals.

My thesis on QHC was very simple.

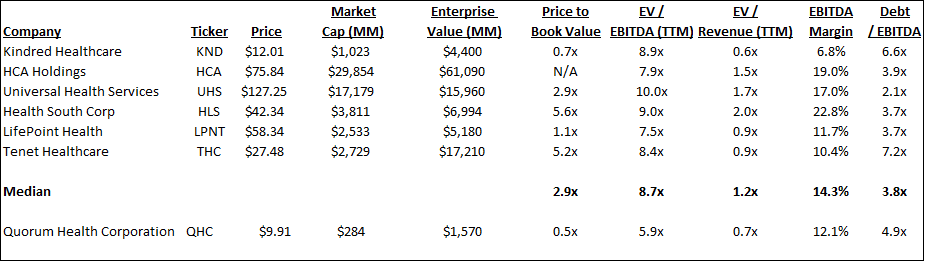

After the spinoff, QHC declined to ~$10 stock price which translates to a market cap of ~$284mm. QHC has $1.3bn of net debt implying an enterprise value of $1.6bn. Management had issued 2016 EBITDA guidance of $265mm to $275mm. Assuming the midpoint of that guidance, QHC was trading at 5.9x EBITDA and very cheap versus the peers that I’ve listed below. The cheapest peer trades at 7.5x EBITDA. This seemed unfair as QHC’s EBITDA margin of 12.1% was slightly lower than peers, but not the absolute lowest. QHC’s debt ratio of 4.9x was higher than median, but not the highest. As such, it seemed that QHC deserved to trade at least in-line with its cheapest peer (LPNT).

Here is how the comp sheet looked prior to QHC’s 2Q results:

Additionally, QHC is in the process of divesting unprofitable hospitals. It has outlined a plan to sell 11 of its 38 hospitals which were EBITDA negative. Management believes these sales would generate $100mm in total proceeds. These proceeds were going to be used pay down debt. These negative EBITDA hospitals lost $8mm in total EBITDA according to QHC’s Form 10. So here was my thinking.

QHC is already cheap, trading at 5.9x EBITDA versus its closest peer trading at 7.5x. Additionally, if QHC is able to complete the sales, it would be able to generate $100mm in proceeds which would be used to pay down debt and EBITDA would increase by $8mm.

So net debt would go from $1,286mm to $1,186 and enterprise value would decrease from $1,572mm to $1,472mm. EBITDA would increase from $270mm (midpoint of guidance) to $278mm. And QHC would be trading (assuming no change in equity value) of 5.3x EBITDA This for a company with a lower debt burden (pro forma leverage multiple of 4.3x down from 4.8x) and a higher EBITDA margin (pro-forma margin of 14.4% up from 12.3%) from divesting negative EBITDA hospitals.

Assuming QHC trades in-line with its cheapest peer, LPNT at 7.5x EBITDA, its enterprise value would be $2,029mm. Back out net debt of $1,186mm leaves an equity value of $843mm. Divide that by 29mm shares yields a stock price of $29.48 versus price at the time of ~$10.

Additionally, there was significant insider buying in the $12 price range in May.

Seemed like a great set up…

What happened next?

On August 10th, QHC reported Q2 earnings:

- Revenue declined 1.6%

- There was a 3.4% decline in total admissions

- Adjusted EBITDA declined by 51% (!!!!)

- 2016 guidance was reduced from $265mm-$275mm to $175mm-$200mm (!!!!)

Investment thesis out the window.

The stock was CRUSHED to ~$4 but has since recovered to $6.12.

Assuming the midpoint of management’s new guidance, QHC currently trading at 7.8x EBITDA. This seems pretty reasonable maybe even expensive considering:

- EBITDA declined 51% in the most recent quarter.

- EBITDA guidance was just reduced by 44%.

- The company’s leverage is 6.9x based on current debt outstanding and new 2016 guidance.

I have sold out and moved on….

Lessons Learned

While hindsight is always 20/20, I gave some thought to my original thesis and analysis to determine if there is anything that I missed.

First of all, on April 8, 2016, QHC announced its senior debt was priced at 11.625%. This is an extremely high rate even for a highly leveraged company. It is telling that creditors demanded this high of an interest rate and implies they viewed there to be significant business risk. Next time I see an interest rate this high, I will have better perspective and think twice before investing in the equity.

Second, there was this question during the analyst meeting in June:

Unidentified Participant:

Okay. Can you sort of go through — you guys had to come out with obviously guidance then the financing you had to talk to us, but I also get the sense as I talk to you that maybe the budgeting process you weren’t fully involved in that when that happened. Where were you at with your comfort level with the guidance that’s out there? And are you in the process of sort of renewing everything so we make come out with the upgrade.

Mike Culotta – Quorum Health Corporation – EVP and CFO

Well, and I will tell you [Wayne]. Wayne has been through a process of this before spinning out in divesting hospitals, and he had asked us up until about a week before May 1st to stay focused on our current jobs and our jobs were helping CHS as possible. And I would tell you this team did that.

We really had the opportunity, May 1st to really — to grab those. And that’s nothing against anybody. That’s just — just was the situation and I think we’re all quick study and trying to make sure what are the TSAs really mean, the transitional services agreements? And what are those costs going to be from CHS.

And we brought over 200 people, did we need 200? Did we need 600? Did we need 100. And those are issues that we have been working through.

We’re feeling much more comfortable today than we did May 2nd. I will [share] you that, we didn’t know what was going on. We have never closed the books on these hospitals until the end of May. And needed CHS’ help on it with the resources that they had. Everyday we get much more comfortable in being able to. We’ve got really good people, really talented people. We just want to get a little more familiar with the hospitals and with the nuance associated with setting up a budget.

So our Board has been very supportive with the fact that we didn’t have a budget [day one], and there wasn’t a budget for these hospitals. There was a budget for the hospital. There wasn’t a budget from the overhead corporate office. And my belief is that we go from 7,000 to 200. We should be able to offer some value associated with those hospitals, too. And so we’re trying to do that aspect, too. And how do we help the margins just because we’re different?

My Thoughts

The implication here is QHC management didn’t really sign off on the guidance. I was basing a lot of my analysis on management’s guidance which turned out to be a mistake. In the future, I spend more time independently verifying management’s guidance to determine if it is reasonable.

Conclusion

Obviously every investment does not work out. I’ve cut my loses and will hopefully be able to apply some of the lessons that I’ve learned to future opportunities.

On to the next one!

This is very valuable. Coming from someone who had his finger on the trigger to invest in QHC I really appreciate your rundown on your thought process and where you see that you went wrong. Personally think this is the best way to learn.

Many thanks for the comment, Ben. Yes I definitely learned a lot from this one, and generally feel that I learn the most from my mistakes.

Personally, I wouldn’t count this as a mistake. The set up was there and you went for it (I would have done the same). In my humble opinion, if there was any mistake, it was selling it when it cracked 50%. Perhaps that was the time to really dig in and maybe buy more now that all the bad news was in the price and all the remaining old investors would have panicked and dumped the stock? I know the stock went to as low as 3.75, so I imagine it was tough to hold on!

Just my thoughts. Appreciate your blog (loved the most recent one re superinvestors). Thanks!

Thanks for the comments GB. Yes, perhaps it was a mistake selling after the stock was down 50%! I just didn’t feel comfortable holding my position as it was clear that management didn’t have a good handle on the business. Perhaps, I revisit to see what I missed.