Aptevo (APVO) is a recent spinoff from Emergent Biosolutions (EBS), an underfollowed biodefense company. For reasons described below, Aptevo was sold indiscriminately and is currently trading well below any reasonable estimate of fair value.

Reason for the Spinoff

EBS is a specialty pharmaceutical company that is focused on creating biodefense drugs for civilian and military populations. The majority of EBS’ revenue is derived from BioThrax, an anthrax vaccine. In addition to its biodefense drug portfolio, EBS has spent significant time and resources developing a robust pipeline of oncology and immunology drugs. EBS felt the value of this developmental portfolio (currently APVO) was getting buried within EBS. As such, it made the decision to spin out APVO in order to maximize value both for APVO and EBS, the parent company.

Aptevo Therapeutics

APVO currently has four commercial products in hematology and immunology that are on track to generate $40mm in sales in 2016. In addition, APVO has a pipeline of therapeutic antibodies targeted at oncology and autoimmune disorders.

Current Commercial – Four Products

Stable Legacy Products:

WinRho SDF – this drug is used to treat Immune Thrombocytopenic Purpura (ITP) and also for hemolytic disease of the newborn (HDN).

HepaGam B – this drug is used to treat hepatitis B.

VARIZIG – this drug is used to treat varicella zoster.

WinRho SDF, HepaGam B, and VARIZIG are all legacy products that have been on the market for a long time and have stable revenue. Growth will be driven by price increases (EBS never raised the prices on these products) and expanding sales efforts into new territories.

Newly launched product:

IXINITY – this is a recently launched drug that is used to treat hemophilia B. The drug has a unique dosing regimen that enables hemophilia patients to stay more active. It has had good success with its initial launch and APVO expects continued growth as IXINITY carves out its niche in the market.

Piper Jaffray (only analyst on street that covers APVO) expects revenue to grow from $35mm in 2015 to $80mm in 2019 driven primarily by IXINITY.

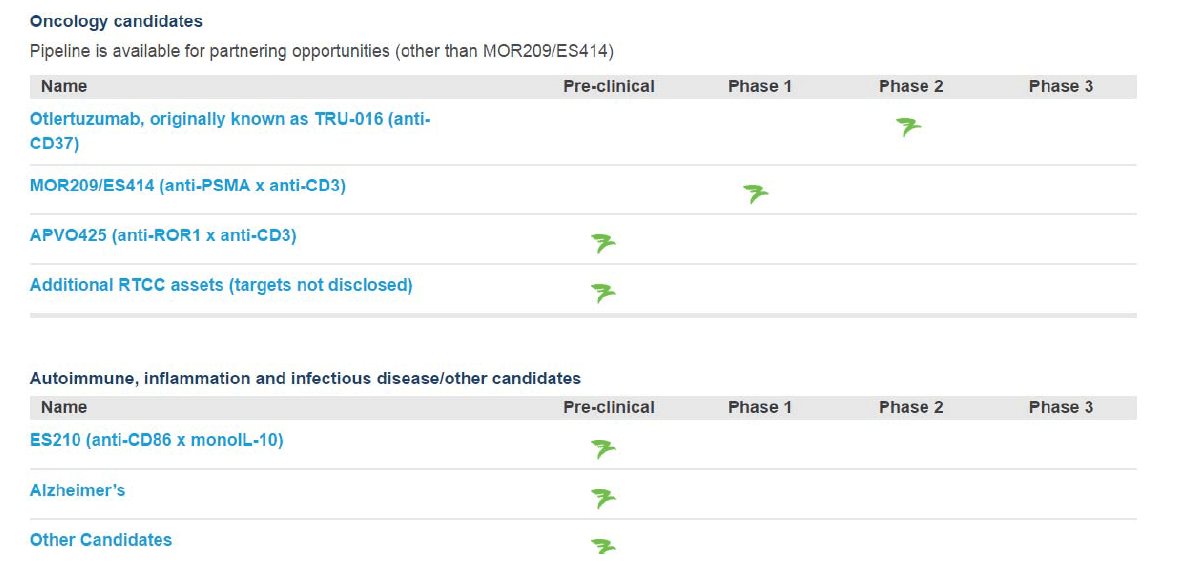

Pipeline

Aptevo has a deep pipeline of drugs that are targeting oncology, autoimmune disorders and Alzheimer’s.

Many of APVO’s drugs in development are bispecific therapeutics. Bispecific therapeutics are antibody-based molecules that are able to bind to multiple targets of therapeutic interest. What does this mean? Well to take a cancer as an example, a bispecific therapy could attack and destroy a cancer tumor while simultaneously stimulating the patient’s immune system to recognize and attack the cancer tumor. Thus the drug could attack the cancer from two different angles.

While I don’t claim to be a biotech expert, bispecific therapeutics is apparently a HOT market.

Recently large pharma and biotech companies have shelled out large amounts of capital to partner with up and coming bispecific companies.

Example #1:

Novartis recently paid Xencor (XNCR) $150mm upfront, plus up to $2.5bn in milestone payments in a partnership on the Xencor bispecific pipeline.

Example #2:

JNJ recently paid Macrogenics (MGNX) $75mm upfront and up to $750mm in total if it hits certain milestones targets.

There are countless others. Just google “bispecific partnerships.”

In APVO, you have an opportunity to invest in a bispecific company for free. After all, the company has a negative enterprise value when you include the $20mm note payable from EBS. Piper Jaffray writes this about APVO: “Many investors have been struggling to identify the best investment opportunity in the group, considering many platforms are either private or buried in much bigger companies. What is unique about APVO is that the valuation, in our view, doesn’t even account for the approved product portfolio, let alone any optionality from the bispecifics…..As a spin-off from a company that many investors don’t follow, it’s flying below radar screens as arguably the best way to invest in the bispecific space.”

From reading APVO’s Form-10 and slide deck as well as talking to investor relations, it is clear that APVO is currently speaking to all the major players in the biotech and big pharma industries about a potential partnership. This would likely come with a major upfront cash payment as well as huge validation. If this were to happen, I believe the stock would trade significantly higher.

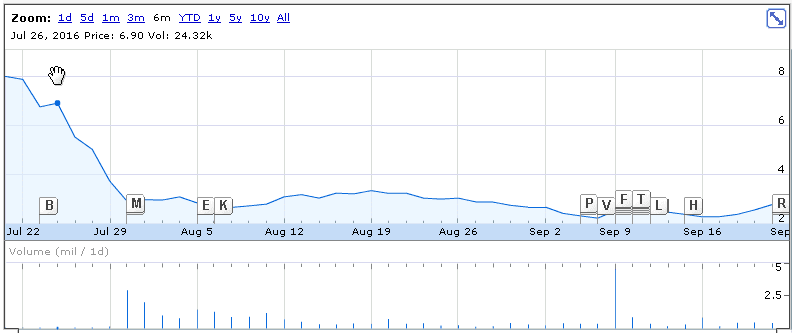

Indiscriminate Selling

As shown in the Google Finance chart below, APVO started trading in the “when issued “market around $8 and has been sold indiscriminately (in my opinion) to its current price of $2.79.

I believe the opportunity exists because APVO was spun off to shareholders that didn’t understand the company and had no interest in owning an unprofitable micro-cap. APVO is a sub $100mm market cap stock and many institutional shareholders have zero interest in holding a micro-cap. EBS was/is a $1bn+ market cap company and so APVO represented a much different type of stock. Additionally, 25% of APVO’s shares were held by indexes which were forced sellers as APVO was not in any indexes. This contributed to the indiscriminate selling.

Valuation

Calgene Acquisition Multiple

One way to think of Aptevo’s valuation is to consider the acquisition multiple that Emergent Biosolutions paid for Calgene. After all, all of APVO’s revenue came from Calgene and APVO’s CFO, chief medical officer and VP of Commerical Operations all came from Calgene. EBS paid $222 million for Calgene which had $127.3mm of revenue at the time, implying an EV / Revenue multiple of 1.7x. Applying the 1.7x multiple to Aptevo 2016 sales of $40mm implies an enterprise value of $68mm. Add net cash (including note receivable) of $65mm yields an expected market capitalization of $133mm. Divide by 20.2mm shares outstanding yields a stock price of $6.58. The stock currently trades at $2.79.

Trubion Pharmaceutical

In 2010, EBS paid $98mm to acquire Trubion Pharmaceuticals. Trubion at the time had a promising pipeline but no revenue. Today, much of APVO’s pipeline comes from Trubion. The transaction provided approximately $20mm in cash, thus, after backing out cash, Trubion was valued at an enterprise value of $78mm. Since 2010, APVO’s pipeline has progressed, but let’s assumes that that $78mm of value is unchanged. Add $65mm of net cash (including note receivable) yields a market capitalization of $143mm. Divide by 20.2mm shares outstanding yields a stock price of $7.08.

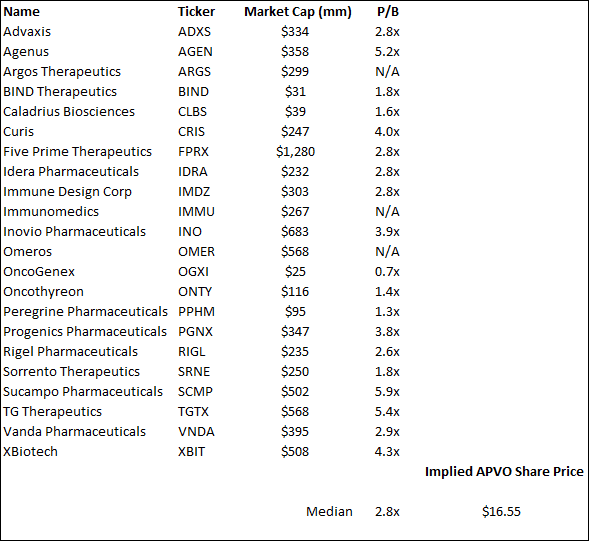

Valuation vs. Other Biotech Comps

On a valuation multiple basis, I looked at APVO versus its peers on a Price to Book Basis and an EV/Revenue basis. For the comp set, I used the group of companies that APVO included in its Form 10 that were listed as peer companies.

Price to Book

Generally pharma and biotech companies trade well above book value due to their substantial intellectual properties driven by R&D and patents. APVO currently trades at 0.4x book value. This is incredibly cheap. As shown below, the lowest comp trades at 0.7x while the median comp trades at 2.8x book value. In the chart below, I’ve shown the share price at which APVO would trade if it traded more in-line with peers.

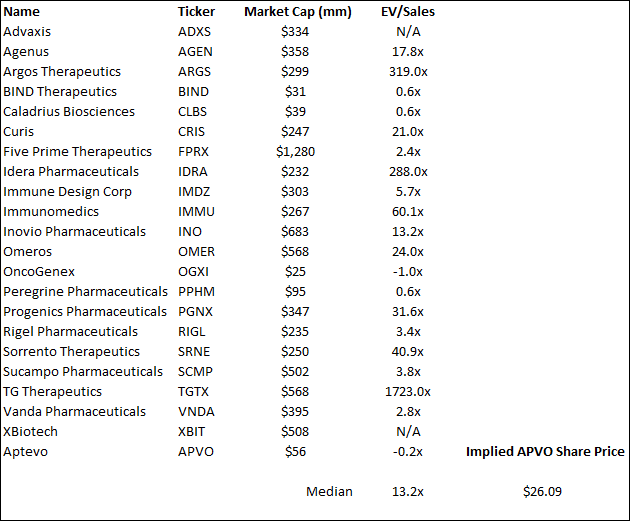

EV / Revenue

On an EV/Revenue basis, APVO also appears dramatically undervalued as shown in the chart below. APVO’s market cap is currently $56mm while it has $65mm (including note payable from EBS) of cash. As such it has a negative Enterprise Value and with $35mm of TTM sales, an EV/EBITDA multiple of -0.2x. If it traded in line with peers, it would trade for ~$26/per share as seen below. It currently trades at $2.79.

Other Points

• Piper Jaffray recently initiated on the stock with a buy and has a target of $7. To quote from the Piper report: “What is unique about APVO is that the valuation, in our view, doesn’t even account for the approved product portfolio, let alone any optionality from the bispecifics.”

• The Edge Consulting Group covers the stock and believes it is worth $6.43.

• Spinoff Research believes the Aptevo is worth an enterprise value of $206mm. Adding $65mm of net cash yields market cap of $271mm and a share price $13.55.

• As a reminder, the stock trades for $2.79.

Conclusion

I think APVO is worth significantly more than its current share price, and I own the stock. The catalyst that would create significant value for Aptevo would be if the company were to announce that it has partnered with a large biotech/pharmaceutical company for the continued development of its bispecific pipeline. This would likely come with a large upfront payment and more importantly validate the platform.

Disclaimer:

I currently own APVO. All expressions of opinion are subject to change without notice, and I do not undertake to update or supplement this report or any of the information contained herein. I have no business relationship with any company whose stock is mentioned in this article. This article is provided for informational purposes. Please do your own work before buying any stock mentioned on this blog.

have you done much looking into insider stakes/incentives here? a potentially very appealing idea here

thank you for the idea

with biotech, i think we should be conservative and estimate the cash won’t last long as the company not profitable.

the annual cash burn is 50m$

it’s more a bet on the value of the pipeline, it’s not really “free”

Very fair point, Francois. I guess my point is that most publicly traded biotechs are not profitable and have large cash burns. Nonetheless, they are valued at valuations (price to book, EV to revenue, etc) that are significantly above where APVO currently trades. In my opinion, there is no reason why APVO deserves to trade at such a discount. The only logical reason I can think of is that APVO was spun off to investors that didn’t care or have any interest in learning about APVO’s pipeline.